Why You Should Raise Your Credit Limit, When You Don't Need the Money

I increased my credit limit by $1,400 this morning, and it took the better part of one minute.

Who knew something so potentially tricky -- asking your bank to potentially lend you a substantial sum of money -- could be so easy? Well, it is. And not only is it easy, it can be very important for your credit score. Here's why.

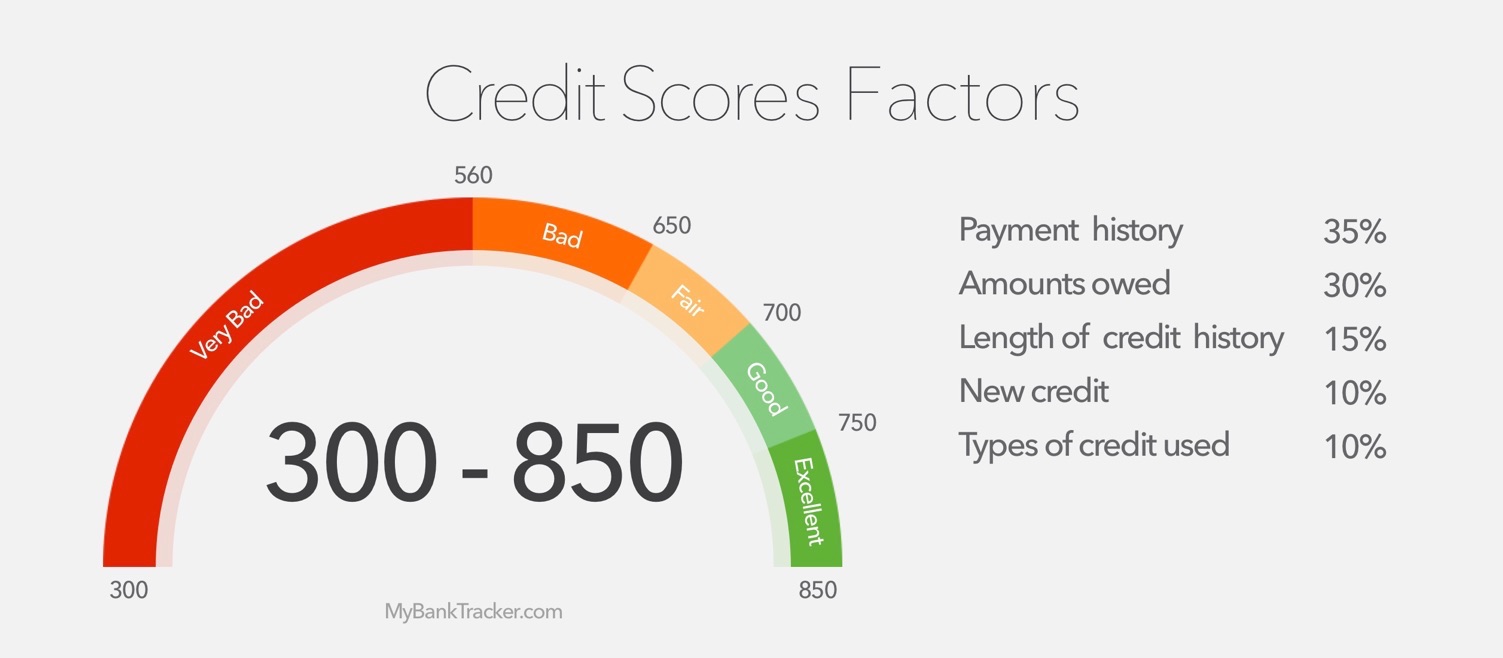

How FICO Score is Calculated

Your FICO score is based on five metrics, each weighted differently: payment history (35%), amounts owed (30%), length of credit history (15%), new credit (10%) and types of credit used (10%).

Unlike in college, where professors offer their grading schemes on your syllabus on the first day of class, your credit card issuer is not required to educate you about how your score is determined.

You might reasonably assume that payment history is the most important part of your score, and you'd be right, but it makes up a mere plurality of the total score.

The amount of your revolving lines of credit that you use matters 30% -- just 5% less than payment history, making the difference between the two nearly negligible. But this isn't exactly intuitive.

After all, if you pay your balance down, who cares if you max out your cards every month?

Card-maxing, however, is generally a habit of those who do not pay their bank back for the money they've borrowed, or who do so very slowly anyway, or through debt consolidation -- it doesn't signal that you're in control of your finances, and that is what your credit score is all about.

It's shorthand for lenders and underwriters who need to know what sort of borrower you are, but don't have the time to get to know you.

And because your credit score is updated at irregular intervals, generally speaking, you want to keep your balance low especially if you use your card to finance larger purchases.

How Much Credit Card Balance You Want to Carry

For all the personal-finance bloggers who insist that credit cards are only practical when paid off in full at the end of every month, there are probably thousands of Americans who use their cards to finance larger purchases and manage their monthly cash flow.

There's nothing necessarily wrong with that -- you'll spend money on interest, and your credit won't be perfect -- but you certainly don't want to be carrying a large balance.

In fact, most experts say that 30% of your limit is the highest balance you want to carry on your card.

If you're still using your first credit card, this might be a painfully and impractically low number.

Unlike in college, you have a job that actually pays you money now, and you can spend the money on stuff you want, specifically the things that get you far away from your job: airplane flights, hotel rooms, rental cars, etc.

But you won't want to use your credit card to cover a weekend getaway if it might damage your credit score, needlessly.

If you're at that point in your life, you might consider increasing your credit limit.

Counterintuitive as it seems -- won't this just tempt me to spend more money? -- it is good for your credit in the long-run.

I logged on to my bank's website, told them what sort of work I do -- "Other (Not Listed)" -- how much money I make, and how much goes toward my housing costs.

It took all of a minute, and I instantly had access to $1,400 that I don't actually need, don't actually have, and don't actually want.

And that's the point, right there. Credit scoring can be opaque and seemingly arbitrary, but sometimes there is a sound logic to it, even if it isn't intentional.

Raising your credit limit in order to ensure you improve your credit score is an exercise in both planning and restraint.

While I plan to improve my creditworthiness through this counterintuitive measure, I also acknowledge and remind myself that I do not actually want this money -- I don't plan on ever spending it.

Of course, things can never be so simple in the world of credit cards. Because I asked for a credit limit increase, my bank did a "hard pull" on my credit report.

Unlike a "soft pull," a hard pull lowers my credit score, but only temporarily. It's a temporary, minor and inconsequential sacrifice.

After all, I'm not buying a home anytime soon. And in the long run, it should pay off.

Short-term sacrifice -- even an abstract one -- for long-term gain is exactly what managing your finances is all about, anyway. As weird as credit scoring seems, it has its own logic.

Negative Domino Effect

Lenders have decreased credit limits when customers show less activity or when the lender is just reducing the risk of lending to you.

There are numerous reasons you could see your credit limit drop, and not much you can do about it in some cases.

Obviously, you’ll have less purchasing power with a lower credit limit. But one of the less obvious negatives of a lower credit limit is the potential for a lower credit score.

If your line of credit is reduced, you will, at least temporarily, be using a greater percentage of your credit limit — and you might end up owing more.

Because your credit score is partially based on what portion of your available credit you use, carrying a big balance-to-limit ratio could damage your score.

That lower score can do some serious damage to your financial life by making it tougher to obtain loans, including auto, home or additional lines of credit.

What To Do With A Reduced Limit

The first and biggest step to take if you discover your credit limit has taken a hit is to devote a lot of energy to making sure you don’t owe creditors much.

If you align the amount you owe with your less flexible spending limit, your credit score probably won’t suffer.

If you are having a hard time getting your payments in on time or organizing your various credit accounts, speaking with a credit counselor is never a bad idea.

The Federal Deposit Insurance Corporation (FDIC) suggests visiting the National Foundation for Credit Counseling at NFCC.org.

Reasons For Lower Credit Limits

There are a few reasons your card company might slash your credit limit. Some are based on things you can control while others could be out of your hands.

Cutting it close on current limits

If you’re consistently maxing out your lines of credit, don’t be surprised if your credit card issuer takes action.

Defaulting on other payments

When you default a credit card account with any institution, your other credit card issuers could take notice.

Identity theft

If your identity is stolen, your credit could end up in shambles, depending what the thief does with your information and how quickly the problem is resolved.

Credit bureau error

Not every credit-reporting agency is perfect. It’s a good idea to check up on your reports yearly to make sure none of your information is egregiously out of place.