Credit Score vs. Credit Report, How Lenders Examine the Two

Your credit score and credit report go hand in hand, but they are actually two different entities that can impact your finances.

Your actual credit score determines your overall worthiness as a borrower, while your report is a full summary of how you've handled credit within recent years.

Knowing the difference between a credit score and credit report can help you make the right financial decision when it comes to applying for lines of credit, and can also help you get better interest rates on loans.

Someone who wants a quick glance at your current standing can take a look at your score to determine your eligibility for a loan, what interest rate to charge, and how much of a risk you appear to be.

Yet, it is still important to have a solid report, because it is a comprehensive breakdown of your personal credit history and your borrowing habits.

If you have a low credit score, lenders cannot see exactly why. By reviewing your credit report, lenders can see detailed information on when and what accounts showed poor credit behavior.

Credit Scores Play a Vital Role

Think of a credit score as a lender's way to get a glimpse into how you manage to pay your debt down and whether you do so on time.

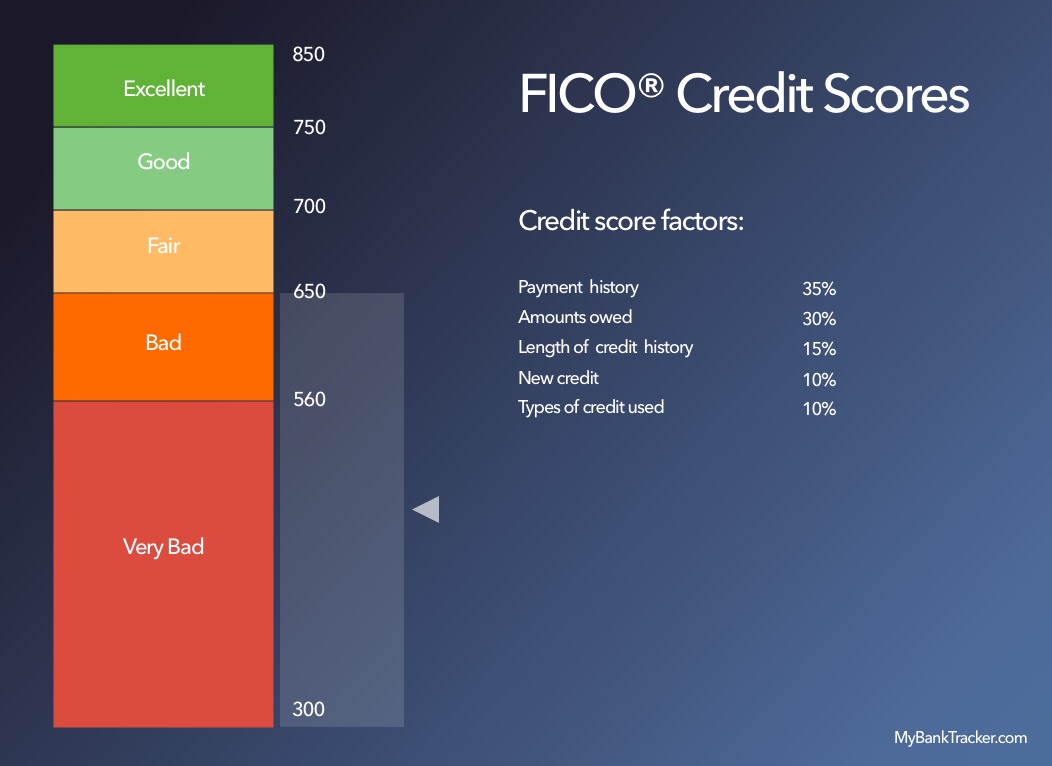

A FICO credit score is the most commonly used credit score by U.S. lenders. It has a range of 300 to 850 -- a higher score means that you are more trusted with credit.

Whenever you get pre-approved for things like credit cards or a mortgage refinance, your credit score is going to determine how a lender treats you.

So, do your best to get your score as high as possible to give a good first impression to lenders.

Having a Solid Credit Report is Essential

You need a solid credit report especially when you're applying for bigger loans such as a mortgage. Your credit report will be pulled up and analyzed in detail.

Lenders will likely review many factors, including these:

- Credit history

- Household income

- Monthly expenses

- Personal assets

You could have a weaker credit score, but if you have made a serious commitment to pay off your debts, that effort can help give you leverage when applying for a loan.

Before a lender hastily rejects you, or offers you a line of credit with high interest, you can show them your credit report.

Inform the lender of your recent effort to pay down your debt -- you may not be aware of it, but you have negotiating power when it comes to taking out a loan, especially if your have recently improved your credit score and report.

Remember to check your credit report each quarter to ensure there are no errors or fraud.