Why Does Your Credit Score Fluctuate Every Month?

Checking your credit score for the first time can be a nerve-wracking experience.

Your credit score is a number that reflects your credit history and profile effects so many financial decisions. Basically, it lets lenders know how much they can trust you with their borrowed money.

When your credit score requested by a lender, the score will reflect the most up-to-date information based on your activity.

It can even change from month to month by a few points, even if you pay off your credit card in full each month and don’t have any debts.

There are many reasons that your credit scores are changing constantly. But first, you have to understand what goes into your credit scores.

How Credit Scores Are Determined

Credit scores become incredibly important when making big life purchases, such as a house or when applying for loans.

Even if you’re young and may not need a loan or are not even thinking about buying a house, your credit score is still something you need to be aware of. The earlier you start working to improve it, the better.

Banks and credit unions use credit scores to make decisions on rates and credit limits when borrowers apply for loans.

People with excellent credit scores have the most options when it comes to taking out loans and get the best interest rates.

Those with poor scores have fewer options and are hit with steeper interest rates. That’s why it’s crucial to keep your credit score as healthy as possible and work to make it higher and higher each year.

Your credit score is created by credit rating companies, such as FICO, or Fair Isaac Corporation, which is used by over 90 percent of major U.S. lenders.

Lenders and banks report your credit actions to credit bureaus, which keep up to date records on your credit history. FICO and other companies, such as VantageScore, base your credit score on your credit history.

While we don’t know exactly how credit scores are calculated, we know of the five main factors that are considered and how much they matter.

The five factors are payment history, the amount of money owed, credit history, new credit and types of credit used. Each has a different weight.

FICO Credit Score Factors and Their Percentages

| FICO credit score factors | Percentage weight on credit score: | What it means: |

|---|---|---|

| Payment history | 35% | Your track record when it comes to making (at least) the minimum payment by the due date. |

| Amounts owed | 30% | How much of your borrowing potential is actually being used. Determined by dividing total debt by total credit limits. |

| Length of credit history | 15% | The average age of your active credit lines. Longer histories tend to show responsibility with credit. |

| Credit mix | 10% | The different types of active credit lines that you handle (e.g., mortgage, credit cards, students loans, etc.) |

| New credit | 10% | The new lines of credit that you've requested. New credit applications tend to hurt you score temporarily. Learn more about FICO credit score |

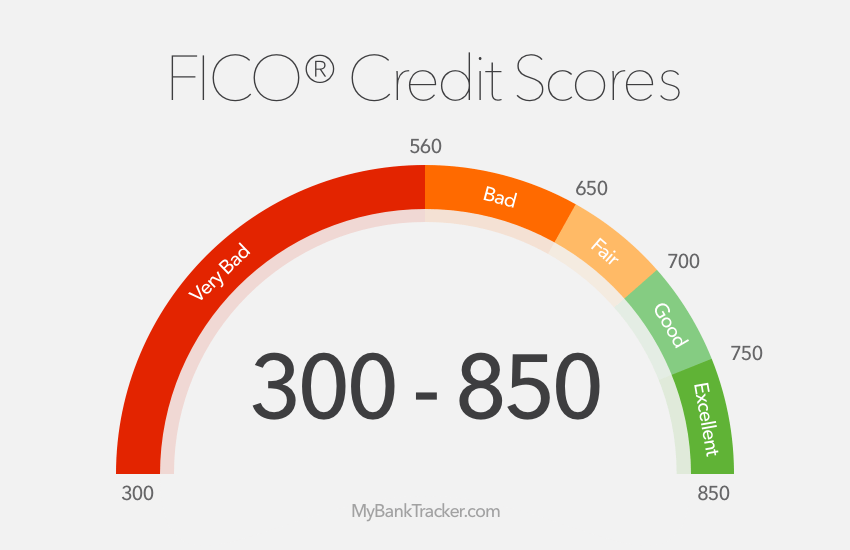

Your credit score is a three-digit number that falls between 300 and 850.

A score between 300 and 560 is very bad, 560 to 600 is poor, 650 to 700 is fair, 700 to 750 is good and anything above 750 is excellent.

You can see how at a certain score range, earning or losing 25 points can take your score from poor to fair or vice versa.

Credit Score Ranges and Quality

| Credit Score Ranges | Credit Quality | Effect on Ability to Obtain Loans |

|---|---|---|

| 300-580 | Very Bad | Extremely difficult to obtain traditional loans and line of credit. Advised to use secured credit cards and loans to help rebuild credit. |

| 580-669 | Bad | May be able to qualify for some loans and lines of credit, but the interest rates are likely to be high. |

| 670-739 | Average/Fair | Eligible for many traditional loans, but the interest rates and terms may not be the best. |

| 740-799 | Good | Valuable benefits come in the form of loans and lines of credit with comprehensive perks and low interest rates. |

| 800-850 | Excellent | Qualify easily for most loans and lines of credit with low interest rates and favorable terms. |

What Time Can Do To Your Credit Scores

Some actions you can’t control, like time. Time, meaning how long you’ve had a credit history, is a large factor in your score.

That’s why the earlier you start, the better off you’ll be by the time you want to buy a house or apply for a loan.

Those with a longer credit history tend to have higher scores compared to someone with only a few years of using credit.

Time also affects each action on your profile. Newer actions, such as opening a new credit account, carry much more weight than older ones.

For instance, opening up a new credit account has a larger impact on a profile with limited credit history compared to one with 20 years of history.

Even though you can’t make the years go by faster to build credit, you can pay your bills on time which is always a positive action.

Late payments will hurt your score. Paying your debts on time as well as paying your credit card in full each month is the easiest and most consistent way to keep your score in great standing.

The Frequency of Score Fluctuations

Like I said before, the effect each action has on your credit score varies.

If you always pay your bills on time, which only reflects positively on your score, you won’t see much change month to month.

However, if you miss a payment or file for bankruptcy, you’ll see a considerable change in your score one month later.

Lenders report negative and positive information to the major credit bureaus in the US, which are Equifax, Experian, and TransUnion. They can report to one, two or all three bureaus each month, but that depends on the lender.

They report information such as punctuality of your payments, account status, account balance, activity by authorized user and recent credit inquiries.

The system isn’t perfect, though. Sometimes there may be a few months between an action and an update to your credit score.

For example, if you pay your credit card off in full, it has to be reported by the creditor to the credit bureau. Once the bureau has updated the information, you’ll see it reflected on your FICO score.

Credit Pulls Have an Effect on Your Scores

There are two types of credit inquiries. One type, called a soft inquiry, doesn’t affect your score at all.

Soft inquiries happen when banks peek at your credit to send you offers for credit cards or loans in the mail. They make sure you qualify before spending money on postage.

The other type is a hard inquiry, which happens when you actually apply for a credit card or loan.

Hard inquiries can shave 5-10 points off your credit score and get added to your credit report. They will be seen by people who do both soft and hard inquiries in the future, whereas soft inquiries don’t get recorded.

Luckily, if you’re shopping around for rates for a new loan there is a period of time where you can do as many hard inquiries as necessary, but it only counts as one inquiry on your report. For FICO, this period lasts 45 days.

Actions such as hard inquiries affect credit profiles differently depending on the range of your score.

For those with excellent standing, a hard inquiry won’t do much damage to a credit score. However, it can really affect those with lower scores.

Higher Credit Scores Can Fall Further

If you have excellent credit standing, meaning your score is 750 or higher, some negative actions will have a much higher impact compared to someone with a fair score.

For example, filing for bankruptcy can knock your score down 240 points if it’s above 750, but will take off half the amount of points if your score is 680.

Of course, the impact of each action varies as well. While filing for bankruptcy or foreclosure has the greatest impact, maxing out your credit card has a considerably lower impact.

Be Careful When Opening and Closing Accounts

Having different types of credit, like a loan and a credit card, is a good thing. Creditors like to see that you can handle different types of debt.

But taking on too much new debt at once is considered a negative action. That’s why it’s best to plan ahead and think carefully about applying for credit cards and loans.

Opening and closing credit card accounts can especially negatively affect your score if you don’t take these factors into consideration.

The more credit you have on each card (the maximum you’re allowed to spend) the better.

On your score, each credit line on your card is combined. Your credit score is affected when you close cards, even if you haven’t used them in years.

For example, if you have two cards that each have $10,000 of available credit but decide to close one, you cut your available credit in half.

Keep in mind, opening up many credit cards at once is not something creditors like to see at all and will lower your score as well.

A fairly easy way to boost your credit score is to contact your credit card companies and ask for more credit.

If you’re in good standing with them, they’ll happily give it to you.

How much credit you use can also raise or lower your score. When it comes to keeping your score healthy, a good rule of thumb is to use below 30 percent of your available credit.

Track Your Credit Scores Carefully

You can monitor your credit score throughout the year for free.

Even if you’re not making important financial decisions any time soon where your credit score would be a deciding factor for banks and lenders, be in the know. That way, you can work to improve your score or keep maintaining it.

Know that based on your activity, it will go up and down. But as long as you pay bills on time and make sound financial decisions, your credit score should only improve.