6 Likely Reasons Why You Experienced a Credit Score Drop

A sudden drop in your credit score can come as a shock. Often it's not clear to you why it happened. What's worse, you may have done something you thought would improve your credit score.

But because of the perverse logic of credit reporting and evaluation, it backfired instead.

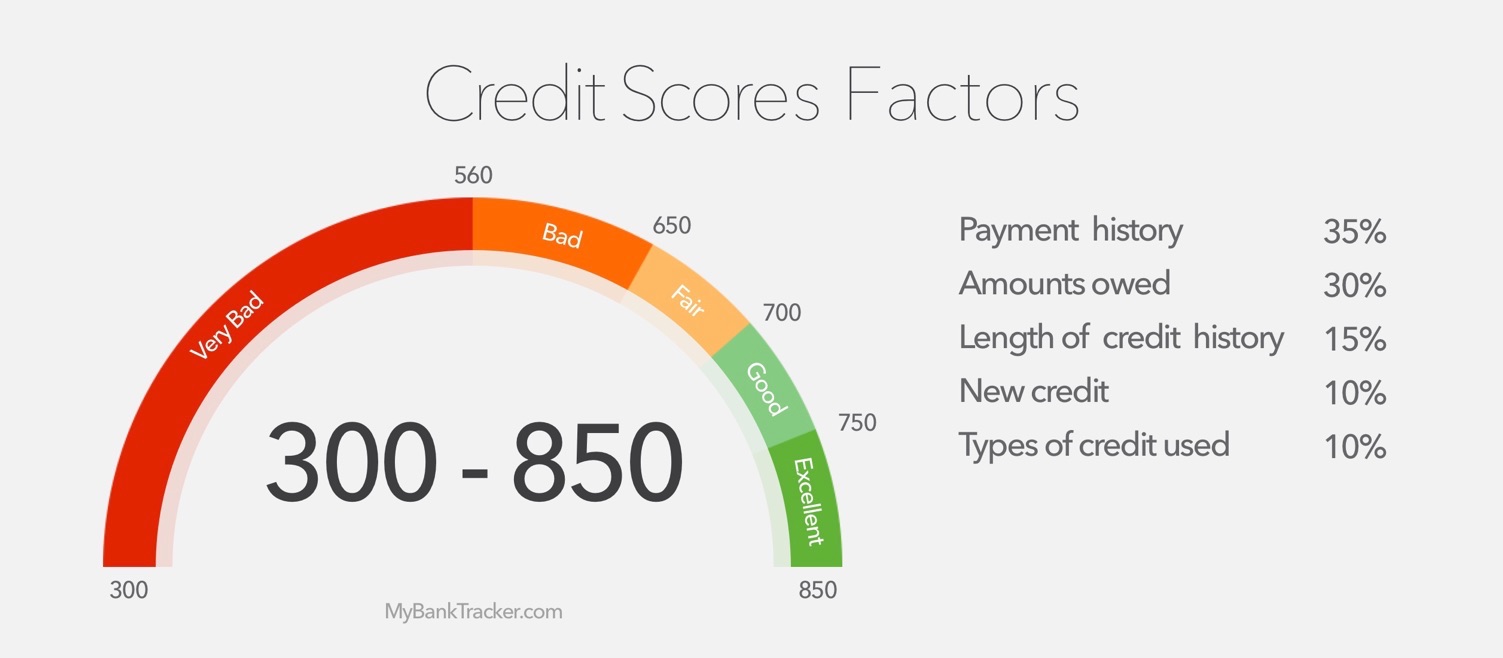

It’s important for you to understand why your credit score dropped. Credit experts tell us your score is comprised primarily of six key credit components.

A drop in your score, they say, can often be traced back to one or more of the following factors -- and they also suggest possible remedies to correct the problems.

1. Derogatory marks on your credit report

If you experienced a major drop in your credit score, a derogatory mark on your credit report could be to blame.

Tax liens, accounts going into collections and bankruptcies are among the most serious things that can happen to your credit score.

Since they represent major delinquencies, they can reflect poorly on your ability to take care of your finances.

Remedy

Check your credit report to see what's in it. Federal law gives you the right to view your own credit report.

You should check it at least once a year to make sure the correct information is being reported.

First get a free credit report from AnnualCreditReport.com. To work on specific accounts, get copies of your credit reports from each of the three major credit bureaus: Equifax, Experian, and TransUnion.

Investigate whether any derogatory marks you find actually belong on your reports.

If you find that these marks are errors, you always have the option to file a dispute. Dispute anything you find in your credit report that is inaccurate, incomplete, out of date, or that you believe cannot be verified.

2. Your credit card utilization rate

Carrying a significant amount of debt on your credit cards could be one reason why your score dropped.

Your credit card utilization rate portrays the total debt you have on your credit cards divided by your total credit limit.

If you're relying too much on credit, a lender could view that as a bad sign.

Remedy: You can try paying down debt, taking on less debt in the future or increasing your available credit on your credit cards by requesting a credit limit increase from your card issuer.

Additionally, if you have been paying your credit cards responsibly, consider opening a new credit card, which will also increase your total available credit. All of these actions will effectively lower your credit utilization rate.

3. The percentage of payments that are on time

Since creditors are trying to judge how likely you are to pay back your debt, reliability is important to them.

If you miss even a single payment, your score could take a hit. The relative impact could be especially high if you've never missed a payment before.

Remedy: If you're not sure which payment you missed, open up your full credit report. Click on the "Accounts" tab, and expand each account to see your 48-month payment history.

Moving forward, you can set up an automatic withdrawal from your bank account, or link your financial accounts and turn on bill reminders to help avoid missing any future payments.

Continue monitoring your credit report as well to ensure all of your future payments are being reported as on-time.

4. The age of your open credit lines

The longer you have had credit accounts open, the more creditworthy you generally appear to lenders.

If you've closed an account recently, some scoring models won't factor in your closed account when determining your credit age, so your credit history may appear shortened and your score might drop.

Opening a new account could also lower the average age of your accounts.

Remedy

Before opening or closing an account, consider how the action could potentially affect your score, and be prepared for a change when you pay off a loan. If you're not sure if you need to close an account, consider the pros and cons of doing so.

5. The total number of accounts

While it's not the most important part of your credit score, having a good mix of different types of credit and an appropriate number of open accounts shows lenders that you have the experience to pay off debt responsibly.

If you've just paid off the only loan you have, your credit mix might look a little less diverse to lenders.

Similarly, if your total number of accounts suddenly skyrockets or nosedives, that could indicate that you're financially strapped and need credit or can't afford your existing credit accounts.

Remedy: Before you open or close any accounts, you may want to check your credit report's "Overview" tab, where you can see the distribution of your open and closed accounts. Doing so will help you be aware of where you stand.

If you're thinking about opening up new credit cards, don't fall for every offer out there -- only open ones that you need.

6. Your hard credit inquiries

Generally when you apply for a new form of credit, whether it's a credit card, an auto loan or a mortgage, a hard inquiry is placed on your credit report.

Normally, a single inquiry would initially only drop a few points off of your score.

However, if you have applied for several accounts in a short period of time, you could appear desperate for credit and the damage from those hard inquiries might add up.

With that said, some scoring models allow for rate shopping on auto or home loans without any additional damage.

Keep in mind, though, that not all scoring models allow for this type of comparison shopping without significantly affecting your credit score.

Remedy: To avoid unnecessary inquiries, only apply for credit cards when you need one (and can afford it) and you should try to focus on cards that you have a good chance of getting approved for.

If you're looking for a loan and need to rate shop, consider looking through consumer reviews before doing so to narrow down your choices.

By doing your homework, you can make an informed decision without becoming a sitting target for several hard inquiries.

Building your credit knowledge

Now that you know what factors could make your credit score drop, try your best to keep an eye on your credit reports and history.

Even though credit pitfalls can't always be avoided, if you use your knowledge to gauge the possible impact of your financial moves -- bad scores won't blindside you and come as nearly the shock they would otherwise.