How to Save Your Tax Refund in Series I U.S. Savings Bonds

Last year, the IRS reported that the agency received 22,520 tax returns requesting over 99,000 savings bonds totaling $11,190,200.

By offering the option to purchase U.S. savings bonds with tax refunds, the government encourages taxpayers to save while it gets to hold on to taxpayer money.

How to Use Your Tax Refund to Buy U.S. Savings Bonds

You can purchase Series I Bonds at face value — you’ll get a $50 I Bond. In a single calendar year, you can buy a maximum of $5,000 in bonds in increments of $50.

For the first $250, you’ll receive up to five (5) $50 bonds. For savings bond purchases over $250, you’ll receive the five (5) $50 bonds and the remaining amount will be issued in the fewest possible denominations of $50, $100, $200, $500, or $1,000.

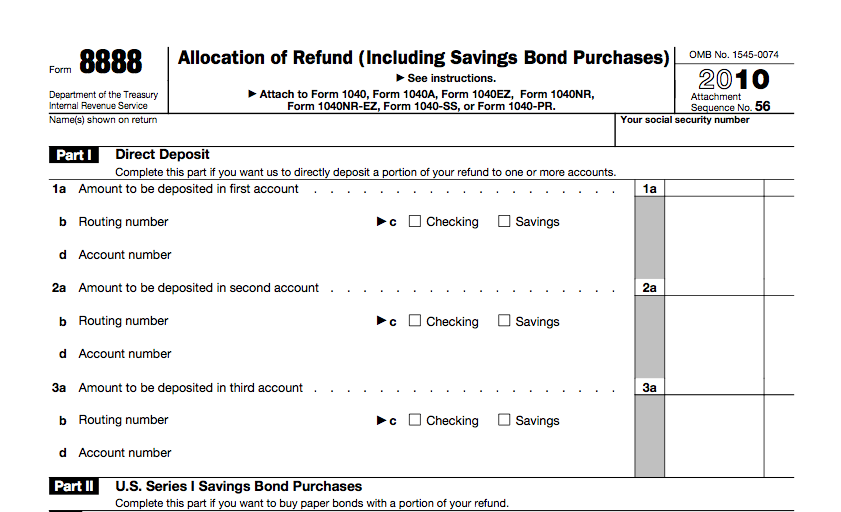

When filing your tax return, notify the IRS that you want to save all or part of your tax refund in savings bonds. Designate how much you’d like to invest in I Bonds by submitting Form 8888, Allocation of Refund (Including Savings Bond Purchases). You can split your refund between direct deposits, paper checks, and savings bond purchases.

Find the best rates

Unlock exclusive savings rates and gain access to top-tier banking benefits.

Savings Bonds vs. Other Savings Products

In early 2010, when the IRS first offering the option to use tax refunds to buy savings bonds, the composite earnings rate was more than four times that composite earnings for early 2011.

Series I Savings Bond Rates 2010-2011

| Period | Fixed Rate | Semiannual Inflation Rate | Composite Earnings Rate |

|---|---|---|---|

| November 2009 – April 2010 | 0.30% | 1.53% | 3.36% |

| November 2010 – April 2011 | 0.00% | 0.37% | 0.74% |

On January 8, 2010, the national 5-Year CD rates average was 2.55% APY, which was unable to top the 3.36% composite earnings rate. As of February 14, 2011, the national 5-Year CD rates average is 2.04% APY, which now beats the 0.74% composite earnings rate. High-yield online savings accounts from popular Internet bank such as ING Direct and Ally Bank are currently offering 1.10% APY and 1.09% APY, respectively, which offers better returns than the current rates from Series I savings bonds.

Aside from the currently low earnings rate, a concern involving the physical nature of paper bonds may dissuade taxpayers from buying savings bonds. It requires careful safekeeping unless bond holders put them in safe deposit boxes or convert them to electronic bonds in a TreasuryDirect account.

The neat feature of I Bonds is the variable semiannual inflation rate. Assuming that interest rates will rise, I Bonds can be viewed as CDs with interest rate bump-ups every 6 months rather than locking in money at a fixed rate for the duration of the savings product.

Learn more about using your tax refund to buy U.S. savings bonds by visiting the IRS website.

Will you be buying U.S. Series I savings bonds with all or part of your tax refund this year? Let us know in the comments section below.