4 Times You Shouldn’t Pay Off Your Student Loans Early

When you’re buried in student loan debt, unloading it as quickly as possible seems like the obvious choice. While there are some emotional and financial benefits to paying off student loans faster, there may be a better way to put your money to work.

Should you be paying off student loans at warp speed, versus using the extra money to earn a higher return through investing?

Even if you’re not at the point where you’re ready to dive into the market, are there any scenarios where devoting every single penny to your student debt is actually the wrong move? We think that for some grads, the answer is yes.

Here are four times when knocking out those loans right away doesn’t always make sense.

1. You’re Not Maxing Out Your Retirement Savings.

Millennials are hyperaware of the need to start saving early for retirement, but they don’t always practice what they preach.

According to this study, the lowest demographic who actively participate in a retirement plan are those aged 26 to 34 at only 46%, whereas the highest demographic to actively participate in a retirement plan are those aged 55 to 64 at 60%.

When it comes to taking advantage of the power of compound interest, you’re a lot better off socking away money early on in your career rather than later.

Let’s say you’ve have roughly $30,000 in loans, which is about the average amount grads owe according to the CollegeBoard.

Your regular payment is $300 and your interest rate is 5 percent. If you double up your payments, you’d cut your payoff schedule from 10 years to 5 and save yourself around $5,000 in interest.

Now, assume that you took that extra $300 per month and funneled it into your 401(k) instead, where it sees a 5 percent annual growth rate.

After 10 years, your student loans would be paid off and your savings would be worth a cool $45,000, not including any matching contributions your employer puts in.

When you subtract the $9,000 you paid in interest on the loans, you’ve still come out $36,000 ahead.

Even if you do not contribute the maximum to your 401(k), it’s important to start contributing something,

Savings Calculator

Powered by MyBankTracker

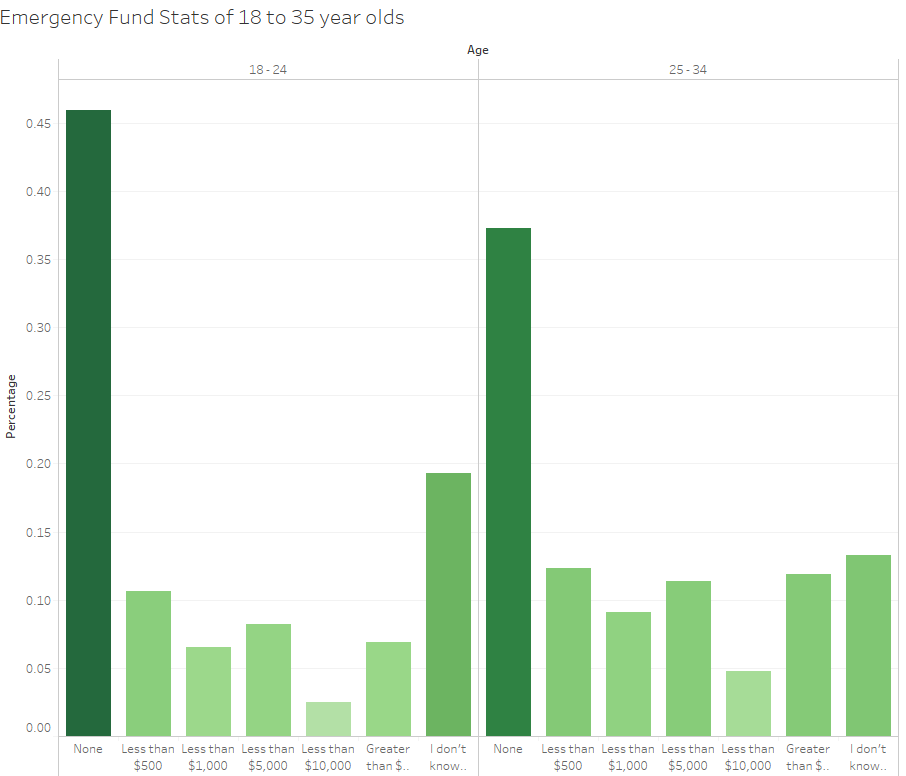

2. You Don’t Have Any Emergency Savings.

Throwing all your extra cash at your student loans can speed up your progress but what happens if you end up losing your job or your car breaks down?

According to a recent study done by MyBankTracker, 56.5% of Americans aged between 18 and 24 have less than $500 set aside for a financial emergency. The scarier statistics that our survey found, is that 36.5 million Americans (about 14.5%) do not even know what an emergency fund is.

If you don’t have any savings to fall back on, you’re going to be stuck between a rock and a hard place when it comes to covering your regular expenses.

In the worst-case scenario, you end up putting everything on a credit card, which only means more debt to deal with later on.

Unless you’ve got a few months’ worth of income saved up, you could be setting yourself up for failure by paying off student loans first.

Using the money you would have put toward your loans to boost your savings account or invest in a CD won’t help you out in terms of reducing the amount of interest you’re paying, but you’ll be glad to have the money when a financial emergency inevitably pops up.

3. You Need an Extra Tax Break.

Twenty-somethings should be cashing in on every deduction they can at tax time, including one for the interest you paid on your student loans.

The deduction, which is good for up to $2,500, reduces the amount of your earnings that are subject to tax so you may end up owing less or getting a bigger refund when you file.

Being able to trim down your taxable income can be especially helpful for millennials who are right on the verge of two different tax brackets.

You don’t need to itemize to write off student loan interest, which is great for young adults who would typically claim the standard deduction.

You can claim the deduction if all of the following apply:

- You paid interest on a qualified student loan in tax year 2019;

- You’re legally obligated to pay interest on a qualified student loan;

- Your filing status isn’t married filing separately;

- Your Modified Adjusted Gross Income (MAGI) is less than a specified amount which is set annually; and

- You or your spouse, if filing jointly, can’t be claimed as dependents on someone else’s return.

For the 2018 tax year, single filers can deduct student loan interest if they make less than $80,000.

The income limit doubles if you’re married and file your taxes jointly.

As long as you’re within the income range and the loans you borrowed were used for qualified higher education expenses, you can benefit from the deduction in a big way.

For now, the student loan interest deduction remains in tact, so make sure to take advantage of it while you can.

4. You’re Not Getting the Best Interest Rates.

One of the most irksome things about paying off student loans is knowing that so much of your money is getting eaten up by interest.

Wiping them out faster will save you some money over the long-term, but there may be a better way to do it than putting even more pressure on an already tight budget.

Federal borrowers can cut their interest rate through consolidation and income-driven repayment programs, whereas refinancing programs are available for private loans.

When you consolidate, you have the opportunity to choose one of the income-dependent repayment plans, which offers a longer loan term.

You can usually extend your payoff when you refinance with a private lender as well.

Consolidating or refinancing can help you get the best rate possible and it also lowers your monthly payment.

If you are considering consolidating your federal loans only, you can do so through the Department of Education.

By applying for federal loan consolidation, you are combining multiple federal loans together to create one monthly payment, instead of having multiple different payments going towards multiple different federal loans.

If you do decide to consolidate just your federal loans together, you will still have the option to apply for loan forgiveness programs, and your interest rate will be determined by averaging out the interest on the loans that you consolidate.

The trade-off is that the loans may cost you more if you don’t pay them off ahead of schedule.

If you’re really committed to getting rid of your loans yesterday, refinancing or consolidating them first ensures that more of your money is going towards the principal instead of being wasted on interest.