What credit score is needed for a personal loan?

A personal loan is an unsecured loan that allows you to borrow a lump sum of money and repay it in fixed monthly installments over a specific period. It is common for borrowers to use personal loans to consolidate debt, cover medical expenses, finance home improvements, or pay for large one-time expenses.

Because most personal loans are unsecured, your credit score makes a huge impact on your ability to get approved and what interest rate you’ll pay. Even a small difference in your credit score can have a significant impact on your monthly payment and total repayment amount.

According to recent industry data, the average American has almost $19,000 in personal loan debt. With interest rates varying widely by credit profile, understanding which credit score is required for a personal loan is essential before applying.

In this guide, you’ll learn how lenders evaluate credit scores, the minimum credit score for personal loan approval by lender type, and steps you can take to improve your chances of qualifying for better loan terms.

How your credit score affects personal loan approval and rates

Your credit score helps lenders evaluate how risky it is to lend you money. Credit scores are grouped together in four major categories: poor, fair, good, and excellent. In general, higher credit scores lead to better approval odds, lower interest rates, and more favorable terms.

Lenders use your credit score for personal loan applications to determine approval and the terms of the loan, which also determine your monthly payment. These terms include:

- Amount borrowed

- Length of repayment term

- Interest rate

- Origination fees

What credit score is needed for a personal loan?

There is no single minimum credit score required for a personal loan because it varies by lender. Most lenders prefer borrowers with scores above 680, but some lenders approve applicants with scores as low as 580. The minimum credit score needed also depends on your income and overall financial profile.

Minimum credit score requirements by lender type

- Traditional banks: 680 or higher

- Credit unions: 650 or higher

- Online lenders: Between 580 and 600

- Peer-to-peer lenders: Requirements vary widely

Remember that you’ll typically receive lower interest rates and fees and qualify for better loan terms as your credit score improves.

Credit score tiers and what they mean for personal loans

Your credit score tier directly affects your approval odds, interest rate, and monthly payment. The higher your score, the lower your borrowing costs are likely to be.

Excellent credit (720–850)

With excellent credit, you have the best approval odds and should qualify for the lowest interest rates and fees from that lender.

According to industry data, the average APR for a personal loan for someone with excellent credit is 10.9%. On a $10,000 loan for three years, your monthly payment would be about $327.

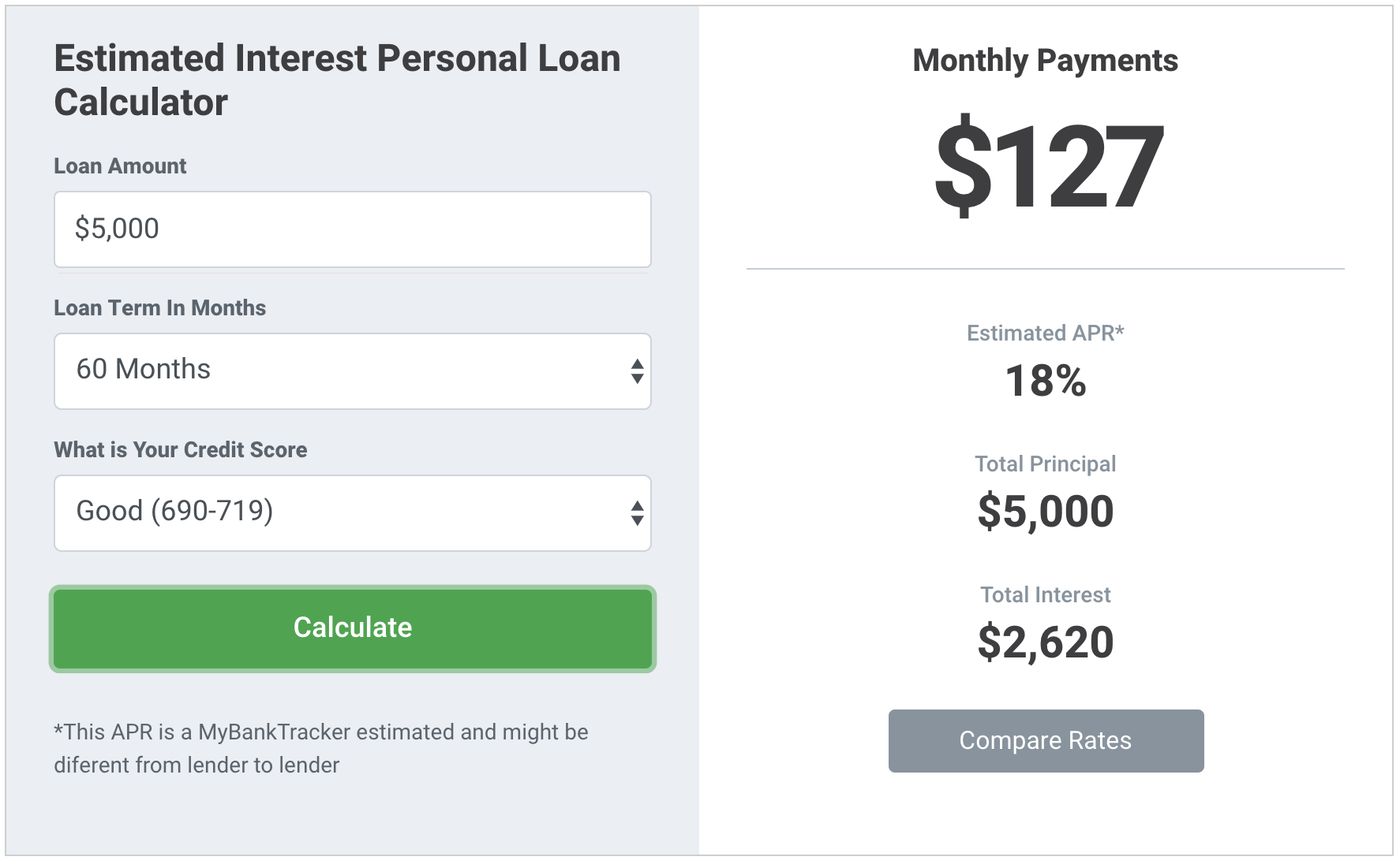

Good credit (690–719)

Many borrowers fall into the good credit range due to a small blemish on their credit report, such as a missed payment or higher-than-normal credit card balances. With good credit, you still have strong approval odds. However, you may pay a higher interest rate or additional fees than someone with excellent credit.

A person with good credit should expect to pay an average APR of 13% for a personal loan. On a $10,000 loan, the monthly payment is approximately $337 for three years.

Improving your score even slightly before applying could help you get a lower interest rate.

Fair credit (630–689)

Fair-credit borrowers tend to have multiple negative marks on their credit reports or may be close to maxing out their available credit. Borrowers with fair credit may have a harder time finding a lender who will approve their loan. When they are approved, the loan terms tend to be more restrictive and charge higher interest rates and fees.

On average, a fair credit score for a personal loan results in a 17.8% interest rate. On a $10,000 loan over three years, the monthly payment is around $361.

To qualify for a better interest rate or lower monthly payment, consider adding a co-signer, extending the loan term, or lowering the loan amount.

Poor credit (below 630)

People with the lowest credit scores often find it hard to get approved for personal loans. The typical interest rate on a personal loan for someone with poor credit is 27.1%. This results in a monthly payment of about $409 on a $10,000 loan over three years.

If you have poor credit, improving your credit score before applying can dramatically reduce borrowing costs.

How to check your credit score before applying

Before applying for a personal loan, it’s important to review your credit report and credit score. While many services charge a fee to provide your credit report and credit score, you can get them for free if you know where to look.

Free ways to check your credit score

- AnnualCreditReport.com: Federal law requires that each of the three major credit bureaus provide a free copy of your credit report once per year.

- Your bank or credit union: Many banks and credit unions provide free credit scores to customers through their mobile apps and online banking.

- Credit bureaus: Experian, Equifax, and TransUnion now provide free access to credit reports and credit scores.

- Credit monitoring services: Tools like CreditWise from Capital One offer free access to credit scores and reports.

Keep in mind that the score you see may not exactly match the score a lender uses, but it provides a general estimate of where your score stands.

What to look for in your credit report

- Accounts you don’t recognize

- Significantly incorrect balances or payment history

- Duplicate accounts

- Outdated negative impacts

If you find inaccuracies, dispute them with the credit bureau before applying for a personal loan.

Will checking it affect your credit score?

Checking your credit score is usually considered a soft inquiry and will not impact your score. When you apply for a personal loan, the lender will access your credit report as a hard inquiry, which can temporarily lower your score by a few points.

You can minimize the impact on your credit by seeking prequalification from lenders before submitting a full application. Prequalification usually only requires a soft inquiry.

Quick ways to boost your credit score

- Pay down debts: Credit utilization makes up 30% of your credit score. Keep balances below 30% of credit limits.

- Make all payments on time: Set up automatic payments to avoid late fees and negative marks.

- Avoid unnecessary credit inquiries: Each hard inquiry can reduce your score temporarily.

- Become an authorized user: Joining a trusted person’s account may boost your score.

The loan application process and credit score impact

Prequalification vs. application

Some lenders offer prequalification that uses a soft inquiry and doesn’t affect your score. A full application requires a hard inquiry, which may temporarily lower your score.

Understanding the approval decision

After submitting a formal application, lenders review your credit score, income, debt obligations, and financial health.

If approved, review:

- Annual percentage rate (APR)

- Loan term

- Monthly payment

- Origination fees and other charges

Final thoughts: Improve your credit before you apply

The minimum credit score for a personal loan varies by lender. In general, the higher your score, the more likely you are to be approved and receive the best interest rates and lowest fees.

Check your credit report for errors and take steps to improve your score before applying. Compare lenders to find the best loan terms for your credit profile.

Frequently asked questions

What credit score do I need for a personal loan?

The minimum credit score varies by lender. Traditional banks may require 680, while some online lenders may approve borrowers with scores as low as 580.

What credit score do I need for a $5,000 loan?

You may qualify with a credit score of 580 or higher, depending on the lender. Higher scores generally receive better rates and terms.

What is the quickest way to improve my credit score?

The fastest way to improve your score is to lower your credit utilization ratio. Keep credit card balances below 30% of their limits.