Personal loan vs. home equity loan: Choosing the best financing for home improvements

Whether you’re dreaming of a kitchen overhaul or planning to make much-needed repairs to your home, major improvements can boost both comfort and your home’s value. The challenge, of course, is figuring out how to pay for it all without derailing your finances.

For many homeowners, that decision comes down to a personal loan vs. home equity loan. Both options can provide the funds you need to move forward with your plans, but they work very differently and come with their own pros, cons, and risks.

This guide breaks down how personal loans and home equity loans work, their advantages, and who they’re best for. By the end, you’ll have a clearer picture of which financing option makes the most sense for your home improvement goals.

Understanding home improvement financing options

Personal loans and home equity loans can both fund home improvements, but they differ quite a bit when it comes to loan structure, costs and risk. Here’s a closer look at each option and how they compare.

How personal loans work for home improvements

A personal loan is a type of installment loan that provides a lump sum of cash up front, which you repay in fixed monthly payments over a set period of time. When used for home improvements, these loans work quite simply. You borrow the money, complete your project, and repay the loan according to the terms you chose when you applied.

Personal loans typically range from $1,000 to $100,000, although loan limits depend on the lender and your credit profile. This makes personal loans suitable for small to mid-sized remodeling projects, such as kitchen overhauls, bathroom updates, appliance replacements or general repairs.

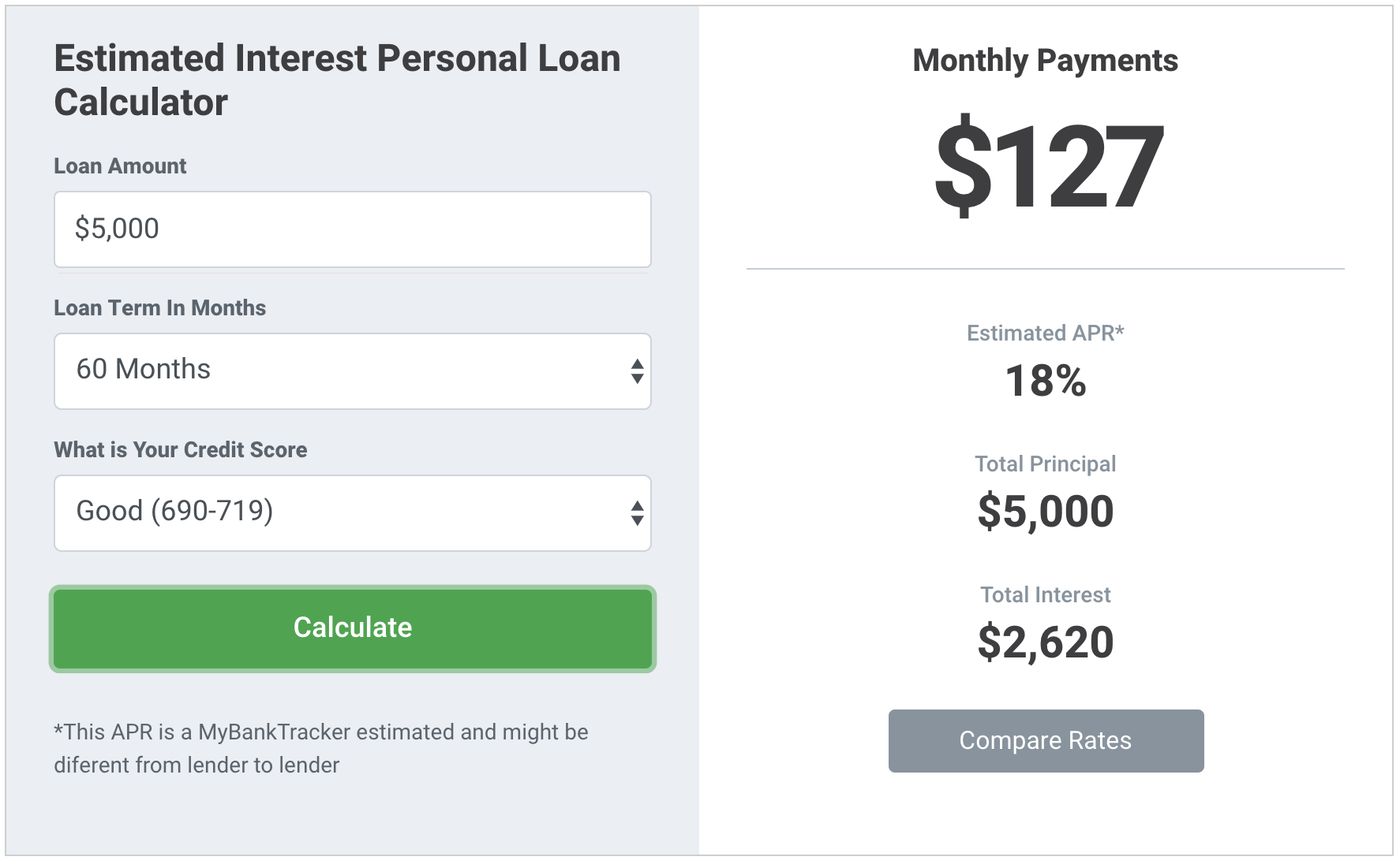

Personal loans are also unsecured, meaning you don’t need to put up collateral like your home or car. Because lenders take on more risk, however, interest rates can vary widely. Current personal loan rates generally fall between about 6% and 36%, with the lowest rates going to borrowers with strong incomes and credit.

Repayment terms for personal loans usually last two to seven years, which is fairly short compared with home equity loans. While this means higher monthly payments compared to longer-term loans, it lets you pay off your debt faster and pay less interest overall.

How home equity loans work for renovations

A home equity loan is a type of second mortgage that lets you borrow against the equity you’ve built in your home. Equity is the difference between your home’s market value and what you still owe on your primary mortgage.

Loan amounts are based on available equity, with many lenders allowing you to borrow up to about 85% of your home’s value when combined with your existing mortgage balance. This often makes home equity loans a better fit for larger or more expensive renovation projects, such as room additions or major structural upgrades.

Unlike personal loans, home equity loans are secured by your home. This reduces the lender’s risk and allows them to offer lower rates. Home equity rates often fall in the 5% to 7% range, although they can vary based on market conditions, your credit score, and your home’s loan-to-value ratio.

Home equity loans also offer longer repayment terms that can last up to 30 years. This can significantly lower your monthly payment, but it also means you may pay more in interest over time. The fact that your home is used as collateral for home equity loans means failing to repay can lead to foreclosure.

Key differences between personal loans and home equity loans

The table below highlights the fundamental differences between personal loans and home equity loans for home improvements:

| Feature | Personal loan | Home equity loan |

|---|---|---|

| Collateral required | No | Yes (your home) |

| Typical loan amount | $1,000 to $100,000 | Based on equity (typically up to ~85%) |

| Interest rates | 6% to 36% | 5% to 11% |

| Repayment terms | 2 to 7 years | 5 to 30 years |

| Risk to home | None | Home is at risk if you default |

Beyond these basics, timing and impact matter. Personal loans usually offer faster approval and funding, sometimes within a few days, since they don’t require a home appraisal or lengthy underwriting. Home equity loans often take longer to close (often 30 days or longer) due to appraisals, title work and additional documentation.

As you decide between home equity loan vs. personal loan, you should also consider the impact on homeownership. Personal loans leave your mortgage untouched, while home equity loans increase your total mortgage debt and reduce the equity you’ve built.

Interest rates and loan term comparison

While personal loans and home equity loans can both deliver the funds you need, the way rates are set — and the extra costs attached — can make one option far more affordable than the other depending on your situation.

How current interest rates compare

Personal loan rates can vary dramatically, from single digits for borrowers with excellent credit to well into the double digits for those with weaker credit profiles. Home equity loan rates are typically more clustered and usually sit several percentage points below personal loan averages.

Note that your credit score plays a critical role in determining rates for both options, but its impact is often more pronounced with personal loans. Since personal loans are unsecured, lenders rely heavily on your credit score, income and debt-to-income ratio to assess risk. With home equity loans, strong equity and a lower loan-to-value ratio can help offset a less-than-perfect credit profile, although good credit is still important.

Another key consideration between these loans is whether they come with fixed or variable interest rates. Most personal loans feature fixed rates, which means your monthly payment stays the same for the life of the loan. Home equity loans usually have fixed rates as well, making them predictable and easy to budget for.

However, some lenders may offer variable rate options, especially through a similar product called the home equity line of credit (HELOC). Variable rates may start lower but can increase over time, adding uncertainty to long-term repayment costs.

Fee and additional borrowing costs

In addition to interest rates, various loan fees can significantly affect how much you actually pay to borrow. Personal loans often charge origination fees that can range from 1% to 10% of the loan amount. These fees are typically deducted from your loan proceeds upfront, meaning you receive less cash than you borrow while still paying interest on the full amount.

Home equity loans usually come with closing costs, which typically range from around 2% to 5% of the loan amount. These costs can include appraisal fees, title searches, recording fees, and lender charges. Some lenders advertise low or no closing cost options, but those costs may be rolled into the loan through a higher interest rate.

It’s also important to watch for hidden fees with both loan types. Personal loans can include late payment fees, prepayment penalties, or returned payment fees, depending on the lender. Home equity loans can come with additional charges for appraisals, document preparation, or early payoff, especially if the loan is closed within a short time frame.

Finally, consider the tax implications. Interest paid on a home equity loan may be tax-deductible depending on current IRS guidelines and your situation. However, this is only helpful to you if you itemize when you file your tax return. Meanwhile, personal loan interest is never deductible in any scenario.

Can you qualify? Approval requirements compared

As you weigh the pros and cons of a personal loan vs. home equity loan, it’s important to understand what lenders look for during the approval process. Qualification standards differ between these options, and knowing where you stand can help you avoid surprises and focus on the financing you’re most likely to secure.

What credit score is needed for home improvement loans?

Personal loan credit requirements tend to be more flexible than requirements for home equity loans, but rates vary widely by lender. Personal loan companies will typically approve borrowers with credit scores of 600 or higher, although competitive interest rates are typically reserved for those with good to excellent credit. Because these loans are unsecured, lenders place heavy emphasis on credit history, payment behavior, and overall credit utilization.

Home equity loans usually require a slightly higher credit threshold, with many lenders looking for a minimum score of 620 or above. Some lenders prefer even higher scores to offer the best rates and terms. Since the loan is backed by your home, your credit score still matters, but it’s evaluated alongside other factors such as equity and loan-to-value ratio.

For both loan types, lenders also evaluate your income and debt-to-income (DTI) ratio. A steady income demonstrates your ability to make monthly payments, while a lower DTI shows that your existing debts won’t overwhelm your budget. Generally speaking, lenders prefer a DTI below about 43% across both loan types.

Home equity loan requirements

Home equity loans come with additional criteria tied directly to your property. The first step is calculating your available equity, which is determined by subtracting your current mortgage balance from your home’s estimated market value.

Lenders typically require a home value assessment to confirm the current value of a property, such as a professional appraisal or automated valuation model. This process helps the lender determine how much you can safely borrow and whether the property meets their lending guidelines.

Ownership duration can also play a role. While there’s no universal minimum, some lenders prefer that you’ve owned your home for at least a year, giving time for equity to build and property values to stabilize.

A key concept in this process is the loan-to-value (LTV) ratio, which compares your total mortgage debt to your home’s appraised value. Many lenders cap the combined LTV at around 85%, meaning you must retain at least 15% equity in your home after borrowing. A lower LTV typically improves your chances of approval and helps you qualify for better interest rates.

Home equity example: If you own a home worth $400,000 and currently owe $200,000, you have 50% equity and a 50% LTV. If a lender is willing to let you borrow up to 85% of your home’s value across a first and second mortgage, you may be able to access up to $140,000 in new funding.

Benefits and drawbacks of each loan type

Choosing the right financing for home improvements isn’t just about rates and eligibility — it’s also about understanding the practical advantages and limitations of each option. Here’s a closer look at what makes personal loans and home equity loans appealing, and their potential drawbacks.

Personal loan advantages and drawbacks

Pros:

- Faster approval and funding: Personal loans can often be approved and funded within one to seven days, making them ideal for projects with tight timelines.

- No risk to homeownership: Since they are unsecured, your property isn’t at risk if you encounter financial difficulties.

- No home equity required: Borrowers don’t need to have equity built up in their home, which is helpful for newer homeowners.

- Flexibility in use of funds: There are typically no restrictions on how the money is spent, giving you freedom to fund your project and other goals as needed.

Cons:

- Generally higher interest rates: Unsecured status means personal loan rates are often higher than those for home equity loans.

- Lower maximum loan amounts: Personal loans usually top out around $100,000, which may be insufficient for large renovations.

- Shorter repayment periods: With terms of two to seven years, monthly payments may be higher than longer-term options.

- Potentially higher monthly payments: Shorter terms and higher rates can make monthly obligations more burdensome.

Home equity loan advantages and drawbacks

Pros:

- Lower interest rates: Secured by your home, these loans typically offer lower rates than unsecured personal loans.

- Higher borrowing limits based on equity: Loan amounts can be substantial, often allowing access to hundreds of thousands of dollars, depending on your home’s value.

- Longer repayment terms: With terms ranging from five to 30 years, monthly payments can be more manageable.

- Potential tax benefits: Interest may be deductible if IRS guidelines allow, and you itemize when you file your tax return.

Cons:

- Risk of foreclosure: Since your home serves as collateral, missed payments can result in losing the property to foreclosure.

- Longer approval process: Home equity loans generally take two to six weeks to close, which may delay your project.

- Closing costs and fees: Appraisal, title and lender fees can add 2% to 5% to the total loan cost.

- Reduces home equity: Borrowing against your home reduces the ownership stake you’ve built, which can affect future financial flexibility.

Which loan is best for your specific remodeling project?

The right home equity loan vs. personal loan depends on the size, scope, and urgency of your project. Understanding which situations favor each loan type can help you make the best choice.

Ideal projects for personal loans

Personal loans are typically best for smaller to medium-sized renovations, usually between $5,000 and $50,000. They are also ideal for time-sensitive projects where you want funds quickly, or for newer homeowners who haven’t built up much equity yet.

Common uses include:

- Kitchen updates

- Bathroom remodels

- Flooring installations

- Minor exterior improvements

Ideal projects for home equity loans

Home equity loans are more suitable for major renovations over $25,000 or for projects that significantly enhance your home’s value. They work well for long-term home improvement investments where lower interest rates and extended repayment terms make sense.

Examples include:

- Home additions

- Complete kitchen renovations

- Basement finishing

- Structural upgrades or major landscaping

Conclusion

When it comes to financing home improvements, personal loans offer speed, flexibility and no risk to your property, while home equity loans provide lower rates, larger borrowing capacity, and longer repayment options. The best choice for you depends on your project size, timeline, and overall financial situation.