The Best Personal Loans in West Virginia for 2024

Personal loans allow anyone who qualifies to borrow money by signing a loan document. No collateral is needed. That’s why these are often called signature loans.

Unsecured loans typically come with higher interest rates than secured loans. You’ll have to shop around for the best deal to minimize your costs.

This can be frustrating because each lender offers its own differing products. Some focus on profiting from high rates and fees, while others concentrate on providing competitive products and closing more loans.

To help you save time, we’ve analyzed lenders in West Virginia to find the best options you may want to consider. Here’s what you should know.

The Best Personal Loans in West Virginia

These are our choices for the best personal loan lenders in West Virginia, in no particular order:

- Truist

- PNC Bank

- Fifth Third Bank

Truist

Truist’s personal loans usually inform you if you’re approved or denied within 15 minutes of applying. In some cases, money from the loan is available the same day.

Loan amounts start at $3,500 with no origination fees. Interest rates are competitive and fixed.

PNC Bank

Personal loans at PNC Bank don’t charge origination fees, prepayment penalties, or application fees. Loan amounts start at $1,000 and reach as high as $35,000.

PNC offers some of the shortest loans available, starting at just six months. The longest loan offered lasts for five years. They have fixed interest rates and a small rate discount may be available if you set up automatic payments from a PNC checking account.

Fifth Third Bank

Taking out a personal loan at Fifth Third Bank gives you a lot of flexibility. Loan amounts range from $2,000 to $50,000 and loan terms are from 12 to 60 months. Rates are competitive and the bank doesn’t charge closing costs or prepayment fees.

How we picked these personal loans

We looked for the top 50 banks by deposit market share in West Virginia based on the FDIC’s June 2021 data–serving borrowers in cities including Charleston, Huntington, Morgantown, Parkersburg, and Wheeling.

Once identified, we evaluated each bank’s personal loan offerings based on these criteria.

- Interest rates

- Loan durations available

- Loan amounts available

- Fees

Are Online Personal Loans a Good Idea?

In addition to brick-and-mortar lenders, online lenders offer personal loans.

Are online personal loans a better deal, though? It depends.

Online lenders don’t have to pay for physical locations in the communities they serve. This can save them money. Some lenders use these savings to offer more competitive loans, while others use them to pad profits.

More tech-focused

Online lenders use a completely digital experience. Applications are completed online and are often processed by technology. This can provide quick loan decisions in most cases. After approval, it may also lead to fast loan disbursement.

Physical lenders see the benefits online lenders offer and have adapted to compete with them. The best physical lenders offer quick application decisions and loan funding while still trying to provide competitive rates.

Some brick-and-mortar lenders allow you to speak with loan officers. This can enable you to explain your application if you’re in a unique position.

Ultimately, finding the best lender will depend on your situation and what loans lenders offer you. For this reason, you need to shop at both digital and physical lenders before picking the best loan for you.

Picking Your Personal Loan Priorities

Except in rare circumstances, you can’t have the best of everything. This applies to personal loans, too. Instead, you must prioritize the most critical characteristics for your situation. Then, shop for the best loan for you.

For many people, the lowest cost loan is most important. For others, loan length or fund disbursement speed may be the top priority. Here are a few loan characteristics to help you decide what is most important to you.

Loan amount

Loan amounts vary for each lender. The most frequent range tends to fall around $5,000 to $35,000. Other lenders may offer larger or smaller loan amounts, but they’re less common.

Interest rate

Your interest rate is one of the most significant factors in the cost of your loan. Minimizing this is key to keeping your costs low. It won’t always be your top priority, though.

Other factors may be more important.

Still, you should shop for the lowest rate after finding a loan with those other factors.

Fees

The best personal loan lenders do not charge application fees, origination fees, or prepayment penalties. Other fees, such as late fees and returned payment fees, still exist.

Still, some lenders charge these fees.

The most costly fee is often an origination fee, which may be a percentage of the loan amount. A 2% origination fee on a $20,000 loan results in a $400 fee.

Funding speed

The fastest lenders can get your loan funded the same business day you’re approved. This can be key if you need the money quickly to make an upcoming or late payment. Other lenders may take days, a week, or longer to get you funds from your loan.

Loan length

Each lender offers a range of loan lengths. Commonly these are around three to five years. Some lenders offer shorter or longer terms, but you’ll have to look harder for these options.

Interest discounts

Some institutions will discount your interest rate with qualifying activities. The most common example is setting up automatic payments. Some banks may give you a discount if you have a qualifying relationship with them before applying for a personal loan.

What’s Required to Apply for a Personal Loan

Personal loan applications usually ask for the below information. Have it ready before filling out an application to speed up the process.

- Identification (Driver’s license, passport, etc.)

- Proof of address (Utility bill, mortgage statement, etc.)

- Social Security Number

- Income and employment verification (W-2, 1099s, tax returns, etc.)

- Highest level of education

- Reason for loan

- Loan amount requested

- Loan length requested

Ways You Could Potentially Increase Approval Odds

Personal loan lenders want to verify your ability to repay the loan you want and their likelihood of getting repaid. Most institutions use the same general information to make these determinations.

The best part is that you can influence two of the factors before applying. These are your credit score and your debt-to-income ratio.

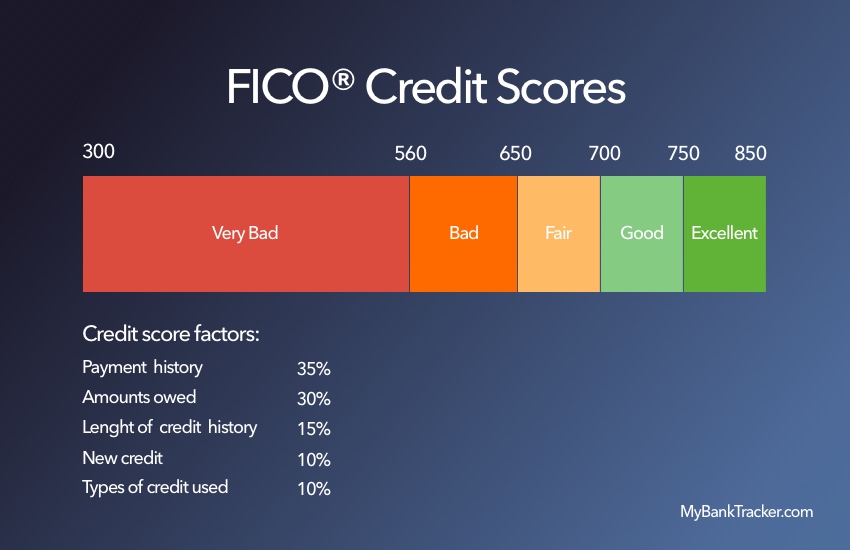

Improve your credit

Your credit score shows your likelihood to repay and is calculated based on information in your credit reports. Before applying, verify that your credit reports don’t have any negative errors.

You can get a free copy of your credit reports from the major credit bureaus at AnnualCreditReport.com. If you find an error, dispute it and get it resolved.

Most credit scoring formulas use your credit utilization ratio as part of your score. It measures the amount of credit you’ve used against your credit limits.

Lowering this ratio could potentially help your score. For instance, it may help to pay down a maxed-out credit card to a more reasonable ratio, such as 30%.

Reduce your debt-to-income ratio

Your debt-to-income ratio measures your monthly debt payments against your monthly income. It helps show lenders how much money you have available to repay a new personal loan.

You can improve this ratio by lowering your debt payments or increasing your income. Reducing debt only helps if your payment changes.

Paying down a car loan or a mortgage with a fixed payment won’t help. That said, paying off one of these loans in full or paying down a credit card with a variable payment would help.

You could also increase your income, but the extra income must be documented. Selling items around your house won’t help, but picking up more hours at work or getting a raise may lower this ratio.

Pick Your Best Personal Loan Option

Finding the best personal loan lender is key to getting the best overall deal. You can speed up the process by considering our top lenders in West Virginia. Once you’ve found your top choice, compare it to online lenders or other lenders you may want to use.

Remember, shopping around for the best terms could save you money. Each lender evaluates risk differently and may offer varying terms.

Frequently Asked Questions

How long does it take to get approved for a personal loan?

After applying, many institutions automatically process applications in seconds or minutes. Your application may take longer if more information is requested or a human review is required.

Other lenders may review applications manually. This could take days, a week, or longer.

How long does it take to receive funds from a personal loan?

Some lenders offer funding the same business day you apply. If funding isn’t received the same day, the next business day is a typical timeline.

Other institutions may take longer, depending on several circumstances. In the worst-case scenario, it could take a week or longer.

Can I use a personal loan for any reason?

Most personal loans don’t restrict how you can use the funds. Some specific personal loans, such as debt consolidation loans, have restrictions. In this example, lenders usually require you to have loan proceeds disbursed to the lenders you’re paying off.

Will applying for a personal loan affect my credit score?

Applying for a loan results in a hard inquiry on your credit report. This commonly results in a slight decrease in your score for a short time.

You may be able to view your rates without formally applying by using a preapproval application. Checking your rate won’t impact your credit score if they use a soft inquiry.