The Best Secured Cards for Rebuilding Credit

When I decided to take the plunge and dive back into credit cards usage (one year after a bankruptcy), I made the mistake of going to my regular bank and opening a secured credit card.

I didn’t do my homework, and it made my life more difficult. I opened the card with my bank because they were already holding my money.

I talked with a personal banker and he assured me that after a review in one year, the bank would upgrade me to an unsecured card. Well, a year of responsible usage later, and they didn’t upgrade me.

The same banker told me I’d have to wait another year. During that time, they got another annual fee out of me.

Another year of responsible usage later, and a different banker told me I’d have to wait one more year.

That’s when I closed the card (and all my other accounts with that bank.) If I’d been smart, I would have reviewed my all my options online before trusting the first bank in mind.

With that lesson learned, I’ve reviewed a slew of secured cards across the internet and compiled a list of the best ones for rebuilding credit and improving your credit score so you don’t have to go through the same thing I did.

Important note: none of these cards is a magic fix. If you obtain a secured credit card to build or rebuild your credit, it will only help you if you use it responsibly.

That means making all of your payments on time and keeping your balance from month to month as low as possible. If you do these things, these cards can be a great tool to help you improve your credit.

Capital One Platinum Secured

The may not offer cash back or travel miles, but what it does offer is pretty spectacular.

Although all secured cards require a cash deposit, not many (or any that I’ve reviewed) allow you to put down a deposit smaller than the credit limit they provide. This card, however, does.

If approved, you may be eligible to put down a $49 deposit and receive a $200 credit limit.

As with all secured credit cards, the more you deposit, the higher your credit limit can go.

However, access to this perk is based on your credit history. If you don’t qualify for the $49 security deposit to get a $200 credit limit, you can still put down $200 and receive a $200 credit limit.

If you use your card responsibly (in other words, making all of your payments on time and keeping your balance as low as possible), Capital One will review your usage every five months.

When they do the review, they’ll check to see if you qualify for a credit limit increase.

When used properly, a credit limit increase can greatly help improve your credit score. (Again, proper usage refers to keeping balances low and always paying on time.)

Read Capital One Platinum Secured Editor’s Review

OpenSky Secured Visa Credit Card

The is one of the best secured credit cards for people who don’t have a bank account.

If you’ve had trouble getting approved for a bank account – of if you flat out prefer not to have one, this card can be a great credit-building tool for you.

While most secured credit cards require you to have a bank account to fund your security deposit on the card, this card only requires that you provide your security deposit through a wire transfer, check, or money order.

So why do most banks want you to have an active checking account before they give you a secured credit card?

For them, it provides more assurance that you have a financial account from which you can pay your bill.

That’s why this card is such a great tool for those who don’t have a bank account. All you have to do is save up for a security deposit and you can get the card you need.

Read OpenSky Secured Visa Credit Card Editor’s Review

Discover it Secured Credit Card

The Discover it Secured Credit Card is one of the best secured credit cards out there because it has no annual fee and you can earn cash back.

These are two features that are rare for a secured card. But, that’s not the only benefit available with this card.

Discover will monitor your FICO score, which will help you keep track of your progress in rebuilding your credit.

As you use your card, Discover will review your credit history, income, and possibly other factors to determine your creditworthiness.

After one year, Discover will evaluate your account on a monthly basis to see if you’re ready to be transitioned to a traditional, unsecured credit card.

How Do Secured Credit Cards Work?

Secured credit cards look and work very similarly to a regular credit card.

The biggest difference is that you have to put down a cash deposit to get a secured credit card, whereas you don’t have to do that with a traditional, unsecured credit card.

The money you put down isn’t used to make monthly payments on your card, though. It simply acts as collateral in the event that you default on your payments.

All security deposits are refundable if you decide to close the card. More often than not, your credit limit will be equal to your security deposit.

Like regular credit cards, secured cards report your account activity to the three major U.S. credit bureaus: Equifax, Experian, and TransUnion. Over time, good behavior on your secured card will be recorded and it’ll help improve your credit.

As a result, you’ll be eligible for better credit cards that don’t require a security deposit.

Know What Determines Your Credit Scores

In order to increase your credit score, you have to understand what affects them. Although the exact formula to calculate your credit score is not available to the public, there are five known factors that affect your score:

FICO Credit Score Factors and Their Percentages

| FICO credit score factors | Percentage weight on credit score: | What it means: |

|---|---|---|

| Payment history | 35% | Your track record when it comes to making (at least) the minimum payment by the due date. |

| Amounts owed | 30% | How much of your borrowing potential is actually being used. Determined by dividing total debt by total credit limits. |

| Length of credit history | 15% | The average age of your active credit lines. Longer histories tend to show responsibility with credit. |

| Credit mix | 10% | The different types of active credit lines that you handle (e.g., mortgage, credit cards, students loans, etc.) |

| New credit | 10% | The new lines of credit that you've requested. New credit applications tend to hurt you score temporarily. Learn more about FICO credit score |

Tips to Improve Your Credit Scores with a Secured Card

Generally, you can make significant improvements to your credit score within the first 12 months of responsible usage with a secured card. However, you may be able to progress more quickly with these tips:

Set up automatic payments

By paying your bill automatically, you’ll never have to worry about missing a payment. Ideally, you pay off the entire balance on the card because interest charges are expensive and could lead to hard to get rid of high-interest debt.

Make partial payments before the statement cycle ends

The balance at the end of the billing cycle is what’s reported to credit bureaus. If you manually make payments before the statement cycle ends, you can decrease the balance that is shown to credit bureaus.

Get the highest credit limit possible

If you have the cash to put down a larger security deposit, you’ll end up with a larger credit line. A larger credit line helps your credit score because you’ll appear to use a smaller percentage of your credit line, which looks good to lenders.

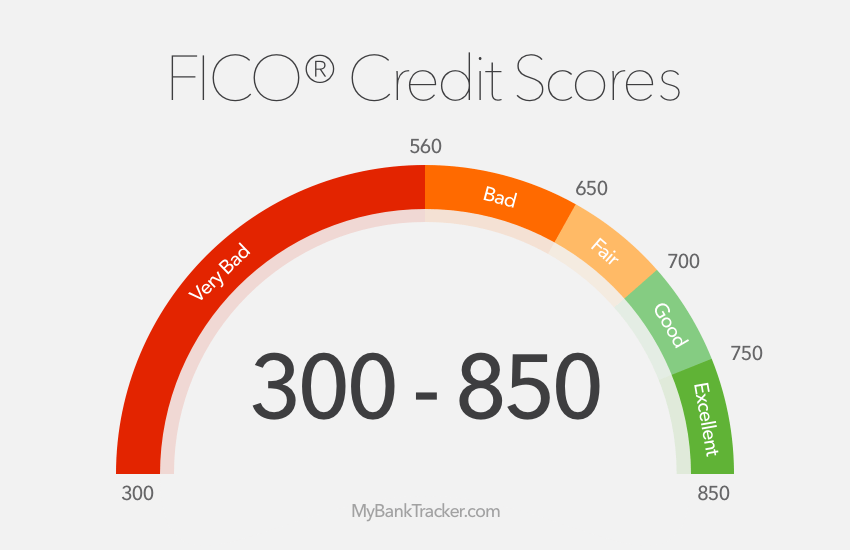

What is a Good Credit Score?

The standard FICO credit score ranges from 300 to 850. The higher your score, the better your credit.

To give you an idea of what your credit scores represent, refer to this chart for a simple breakdown:

Credit Score Ranges and Quality

| Credit Score Ranges | Credit Quality | Effect on Ability to Obtain Loans |

|---|---|---|

| 300-580 | Very Bad | Extremely difficult to obtain traditional loans and line of credit. Advised to use secured credit cards and loans to help rebuild credit. |

| 580-669 | Bad | May be able to qualify for some loans and lines of credit, but the interest rates are likely to be high. |

| 670-739 | Average/Fair | Eligible for many traditional loans, but the interest rates and terms may not be the best. |

| 740-799 | Good | Valuable benefits come in the form of loans and lines of credit with comprehensive perks and low interest rates. |

| 800-850 | Excellent | Qualify easily for most loans and lines of credit with low interest rates and favorable terms. |

A good credit score is at least 700 and you should be able to qualify for credit cards that offer rewards or very low interest rates. For loans, you’re more likely to get approved for the loan and the interest rate is likely to be lower.

A Word About The Secured Cards Listed Here

If I could go back and choose one of these secured cards to help rebuild my credit after bankruptcy, then I wouldn’t have had to do the dance I did with a bank that preferred to string me along than invest in improving my credit-worthiness.

It benefits banks to help their customers. Be a good customer who reads the terms and conditions before applying for products, and always pay on time. Good credit opens doors. Make sure you’re ready to walk through them.