How to Set Up Direct Deposit Without a Voided Check

Direct deposit is a useful payroll feature that lets you get your paycheck deposited directly into your checking account. Instead of getting a physical check each payday, the money shows up in your account the morning that your paycheck is due. This saves you the hassle of having to visit the bank to cash your paycheck multiple times a month.

Often, when you try to set up direct deposit, your employer will ask for a voided check. They use the check when setting up your direct deposit.

Learn why your employer requests a voided check and find out what alternatives you can provide to your payroll department.

Why Do Employers Ask for a Voided Check?

Employers ask for a voided check when setting up your direct deposit because it provides all the information necessary to deposit money in your checking account.

All U.S. banks have routing numbers and all deposit accounts have account numbers attached to them.

Routing numbers are used to identify financial institutions and have been in use for a century. A routing number indicates a specific financial institution, as well as the geographic region of the country it is located in. No two different banks can have the same routing number.

Account numbers identify specific accounts at a financial institution. No two accounts at the same bank will have the same account number.

It is possible for different banks to assign the same account number to different accounts. Because the banks have different routing numbers, your payroll department won’t have trouble sending your paycheck to the right place.

Getting the numbers right

Your employer can identify your specific bank account using just the routing number and account number you provide.

The payroll system will use the bank’s routing number to direct your paycheck to the proper bank. It will provide your account number so the bank can deposit the money into your account.

In theory, you should be able to just provide a routing number and account number to your payroll department. The voided check isn’t necessary, it just happens to have both numbers printed on it.

So long as they copy that information properly, they’ll be able to make the deposit. Still, many companies require that you provide a voided check.

Your company will place the voided check in your file so that it can be referenced in the future if necessary.

For example, if your company changes payroll processors, it may need to provide everyone’s routing and account numbers to the new processor.

Having the voided check on-hand also reduces the likelihood of payroll using the wrong information when it sends out paychecks since they have the check on-hand to reference.

Paychecks deposited into someone else’s account

It’s very important that the payroll department send your paycheck to the proper place. If it winds up in the wrong account, it can be a huge headache to get the money back.

If this happens, the first thing to do is to notify your payroll department. You’ll have to prove that the money never arrived.

Usually, you can just provide a statement that shows the lack of a deposit. Then, your payroll department will need to track where the money was sent.

Then, it will contact the bank that received the erroneous deposit and request that the money be returned. Finally, once the money is returned, your company will send it to you.

This process can take weeks or even months. That’s why many employers are strict about requiring a voided check.

If you do not want to provide a voided check, you can ask your employer for alternate ways to confirm a bank account. You could also ask your employer to make an exception for you if you have specific reasons for not providing the check.

How Can I Get a Voided Check?

Your employer asks you to provide a voided check so that the check cannot be used should it fall into the wrong hands.

If someone gets your checkbook, they may try to write checks against your account. It’s possible that they would succeed, causing money to be removed from your account without your consent.

Voided checks are exactly that: void. They cannot be used for transactions, just like a check that is ripped up becomes worthless.

You can get a voided check in a few different ways.

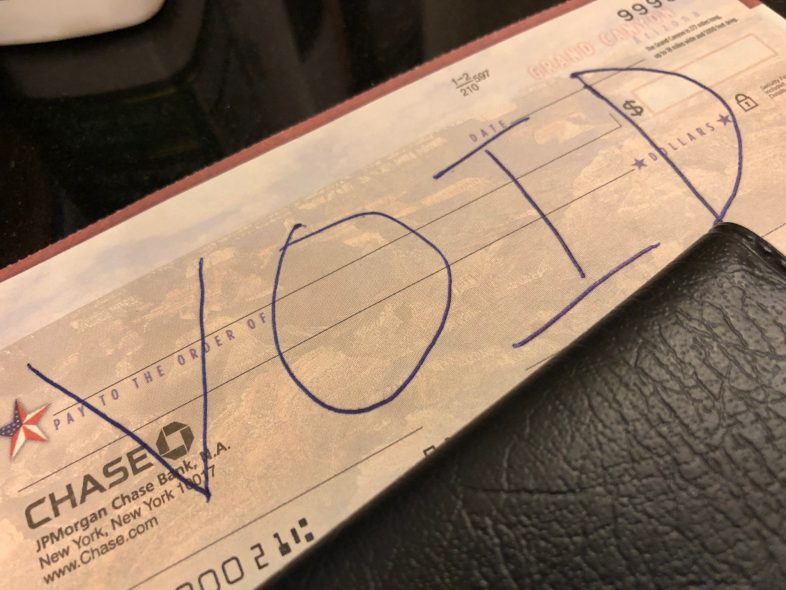

The easiest is to remove a check from your checkbook and to void it. Use a permanent, black or blue pen to write VOID in large letters on the check. Ideally, write it in multiple places, such as:

- The payee line

- The payment amount line

- The payment amount box

- The signature line on the back of the check

- Alternatively, write one large “VOID” that covers the whole face of the check

By clearly writing “VOID” on the check in multiple places, you make it impossible for someone else to use. You can then provide the check to your employer so they can set up direct deposit.

If you don’t have a checkbook, or don’t want to void one of your checks, contact your bank. A teller may be able to print a pre-voided check that you can use to confirm your account. Most banks that operate physical branches will be happy to do this for you.

Setting Up Direct Deposit Without a Voided Check

If for whatever reason, you cannot or do not want to provide a voided check, you still have options.

Direct deposit forms

Many banks, even if they don’t provide pre-voided checks, offer direct deposit forms. These forms are like pre-filled direct deposit forms that you can provide to your employer. They should suffice as proof of your checking account for your company.

Bank documentation

Another option is to ask a teller at your bank for documentation that provides the same information as a voided check. A letter on bank letterhead with your account information could work. All you really need to provide is your account number and the bank’s routing information.

Your account statements

In a pinch, you might be able to provide a copy of a recent account statement. It will include your account number and the name of your bank. You can provide the routing number to your employer who can check it to confirm that it matches the name of the bank on the statement.

It’s worth taking the necessary steps to set up direct deposit because it can save you a lot of time. Another benefit is that many banks charge maintenance fees that can be waived if you set up direct deposit. Setting it up can mean you save a few dollars every month by avoiding bank fees.

Splitting Your Direct Deposit

If you want to get fancy with your money management, or just automate it further, you can split your direct deposits. That means that you can have a portion of your paycheck sent to different accounts.

For example, say that your usual paycheck is for $1,200, but you only spend $1,000 per pay period. You can set up your direct deposit to put $1,000 of your check into your checking account.

Then, you can send the remaining $200 to your savings account. You don’t have to think about the extra money or manually move it to the account.

It just automatically arrives in your savings account and starts earning interest. (We always recommend an online savings account with high interest rates and low fees.)

This makes managing your finances much easier and helps remove the temptation to spend your extra cash. You can use this feature to set up a savings plan.

If you want to save $100 a month to take a vacation, set up a new account for vacation savings. Then set up direct deposit to put $100 per month into the account. At the end of the year, you’ll have the $1,200 you need for your trip.

Most payroll systems let you split your paycheck multiple ways, so you can have money going to three, four, or even more accounts. That means you can use your direct deposit to automate your savings towards multiple goals at once.

Many banks, especially online banks, make it easy to open multiple savings accounts. Each come with their own account numbers.

You can also give each account a name like “emergency fund,” “car fund,” or “holiday savings.” Splitting your paycheck among multiple accounts, each with its own goal makes it easy to save.

Combine that feature with savings plans like 401(k)s that come right out of your paycheck, and you can automate almost all of your required savings. Making sure you don’t overspend and leave nothing left in your account has never been easier.

Conclusion

Direct deposit is incredibly convenient, once you have it set up. You won’t have to worry about losing a check or wasting time cashing it or depositing it. Instead, just go about your life as money constantly arrives in your checking account.

To make things even better, direct deposit doubles as a great way to automate savings. Set up automatic deposits from your paycheck to savings accounts.

Your savings will be separate from your spending cash so you won’t be tempted to spend it, and the balances will grow with each paycheck.

Though it may take some effort, the benefits of setting up direct deposit make it worth doing.