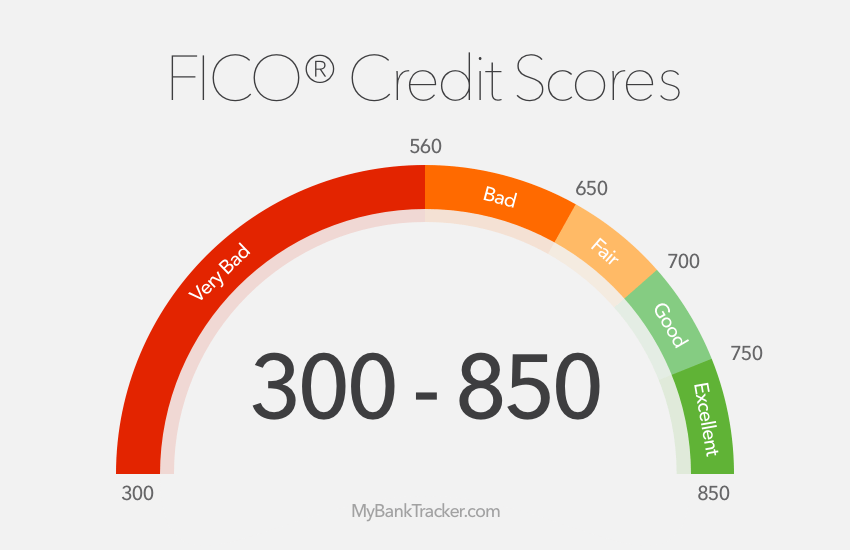

The Best Credit Cards For Very Bad or No Credit History (300-559)

Having no credit history can be such a catch-22. Without credit, you can’t get a credit card or loan.

But you can’t build credit until you’ve shown positive payment behavior on a credit card or loan.

So if you can’t get credit without building it or build it without having it, how are you supposed to get your first credit card?

Since this is a problem that affects many, there are options in place to help. Credit cards for people with no credit history do exist.

They don’t tend to come with a lot of options and rewards – but they do come with more lenient qualification requirements. What’s more, you can use them to build credit until you can graduate on to a better credit card.

The Best Credit Cards for Bad Credit or No Credit

| Card | Best for... | MyBankTracker Rating |

|---|---|---|

| Capital One Platinum Secured | Best for Building Good Credit | 5.0 |

| OpenSky Secured Visa | Best for No Credit Check | 4.0 |

| Deserve EDU Mastercard | Best for College Students | 5.0 |

Capital One Platinum Secured: Best for Building Good Credit

Capital One Platinum Secured Pros & Cons

| Pros | Cons |

|---|---|

|

|

If you have bad credit or don’t have credit, the Capital One Platinum Secured is a great option for you.

This card makes it easy to begin building credit fast. Since it’s a secured credit card, you’ll have to put down a deposit as collateral.The good news is you only need to put down $49 to get started with a $200 credit limit.

There’s no annual fee. Read Capital One Platinum Secured editor’s review.

OpenSky Secured Visa: Best for No Credit Check

OpenSky Secured Visa Card Pros & Cons

| Pros | Cons |

|---|---|

|

|

The OpenSky Secured Visa Credit Card is a great option for those who don’t want their credit getting pulled or those without a bank account.

How can you get a card without a bank account? Well, because this card accepts payments via wire transfer or money orders. No need for a checking or savings account to pay your bill.

There is an annual fee for this card, and the credit limits range from $200-$3,000.

Like the cards above, this is best used as a starter credit card. This card can help you get to a point at which you’ll have even better options in the future.Read OpenSky Secured Visa Credit Card editor’s review.Deserve EDU for Students: Best for College Students

Deserve EDU Student Credit Card Pros & Cons

| Pros | Cons |

|---|---|

|

|

The Deserve EDU Mastercard is a simple student credit card with flat 1% cash back rewards on all spending.Additionally, there are no foreign transaction fees (great for studying abroad too).It also offers cellphone protection (up to $600) when you use the card to pay your monthly cellphone bill.The card has no annual fee.Read the full editor’s review of the Deserve EDU Mastercard.

Credit Card Rules that Affect College Students

College students don’t often have a credit history because lenders prefer not to lend to minors.

In most states, contracts signed by those under 18 aren’t legally binding. Student credit cards are designed to help young adults in school start building credit from scratch.

Student credit cards work the same way as traditional credit cards. The main difference is that there are additional rules that apply to them.

Under the Credit CARD Act of 2009, anyone who applies for a credit card must be at least 21 years old. Otherwise, the applicant must show sufficient proof of income or have a cosigner.

A cosigner can be anyone 21 or older who agrees to share responsibility for repaying any debt on the account.

Many people ask their parents or other family members to co-sign. This is not a light agreement to enter into for anyone. If the primary applicant defaults on their payments, the co-signer has to pay.

How Student Credit Cards Help Build Credit

Student credit card account activity is reported to the three major credit bureaus: Equifax, Experian, and TransUnion.

This means students can benefit from responsible credit card behavior. (The best behavior to show is keeping balances low and making payments on time.)

As long as the credit behavior is responsible, then the student will see growth in their credit score.

FICO Credit Score Factors and Their Percentages

| FICO credit score factors | Percentage weight on credit score: | What it means: |

|---|---|---|

| Payment history | 35% | Your track record when it comes to making (at least) the minimum payment by the due date. |

| Amounts owed | 30% | How much of your borrowing potential is actually being used. Determined by dividing total debt by total credit limits. |

| Length of credit history | 15% | The average age of your active credit lines. Longer histories tend to show responsibility with credit. |

| Credit mix | 10% | The different types of active credit lines that you handle (e.g., mortgage, credit cards, students loans, etc.) |

| New credit | 10% | The new lines of credit that you've requested. New credit applications tend to hurt you score temporarily. Learn more about FICO credit score |

View the factors that make up your credit score in the table above. You might notice a section called “types of credit.” That refers to the fact that having multiple types of credit can improve your score.

If you took out a student loan or if you have an auto loan in your name, then you’ve already been building credit. Then, when you combine that with your new credit card, you’ll be able to increase your score even more.

When you think about building credit for the first time, weigh the costs and benefits. Although you can build credit by using a credit card, it won’t help you if you go into debt on your credit card. In fact, debt hurts your score, thanks to something called “credit utilization.”

Credit utilization is the amount of debt you owe in comparison to the amount of credit available to you.

If your credit utilization is higher than 30%, then your score will go down. (Meaning your card balance is more than 30% of your total line of credit.)

When it comes to credit cards, they only benefit you if you stay out of debt. And, if you carry a balance from month to month, the interest you’ll pay will make it easier than you can imagine to fall into debt.

No matter what type of credit card you start with, always make your payments on time and never carry a balance. Then you can just sit back and watch your financial options grow as your credit score grows.

How Secured Credit Cards Work

A secured credit card is a type of credit card that requires a security deposit as collateral.

The security deposit cannot be used to pay off the monthly bill.

However, the card issuer can seize the security deposit if you default on your payments. Here’s the good news. Because of the security deposit requirement, these cards are easier to qualify for.

Even better, many card issuers don’t pull your credit score when you apply for a secured card.

Basically, the deposit alone does enough to mitigate against the risk of you defaulting.

While you don’t have great credit to get a secured card, a secured card can help you increase your credit score.

All your payment behavior on a secured card will be reported to the major credit bureaus. That enables you to use these types of cards to show positive payment behavior to build credit.

The Security Deposit Determines Your Credit Limit on a Secured Credit Card

With a regular unsecured credit card, the lender decides your card limit based on a few factors. These factors include your income, housing expenses, credit score, and account history.

However, with secured credit cards, your credit limit is equal to your security deposit. If you want a higher credit limit, you have to put more in as your security deposit.

It’s important to note that the security deposit is for your lender, not for you. You can’t just decide to pull your deposit out because you need it. The only way to get your security deposit back is to close the account.

There’s good news, though. Some card issuers will also allow you to graduate from a secured credit card to an unsecured credit card.

You simply have to prove that you’ve been managing your credit responsibly for about a year. At that time you may also be able to get your security back and get a card with higher limits and maybe even some rewards.

This makes a secured card a great stepping stone – and it proves that it doesn’t have to be a forever thing for you.

Annual Fees to Be Expected

Annual fees are no fun, but they’re common in credit cards for people with no credit.

However, there are often ways to have these fees waived. Read the fine print and don’t be scared to negotiate when you open the card – or on the anniversary of opening it. You just might be able to save yourself some money.

The Best Thing You Can Do for Your Credit: Get Started

Starting out for the first time without credit is no fun. It can be frustrating to know you have to work your way up slowly. We all want credit options that can earn rewards and come with more flexibility as soon as possible.

The good news is, this beginning stage doesn’t last forever. Just get started.

Within a few months to a year, you’ll see growth in your credit score. (As long as you use your beginning options responsibly, that is.)