The Best Low-Interest Credit Cards of 2026

Your idea of a great credit card doesn’t have to be one that includes rewards and perks.

Maybe you just want a simple low-interest credit card that minimizes the chances of falling too far in debt.

With hundreds of credit cards available to you, it can be quite a hassle to find the cards with the lowest APRs.

Even then, they can differ in terms of other features.

We analyzed 105 credit cards and we selected three different cards that are likely to match your:

- financial situation

- spending patterns

- debt management habits

Citi Diamond Preferred: Best for an Extended Intro APR Period

Citi Diamond Preferred Card Pros & Cons

| Pros | Cons |

|---|---|

|

|

This card offers a lengthy introductory period on purchases and balance transfers.

It’s also a solid option for those looking to consolidate high-interest debt.

Read the Citi Diamond Preferred Card editor’s Review.

Simmons Visa: Best for Borrowers With Excellent Credit

Simmons Visa Card Pros & Cons

| Pros | Cons |

|---|---|

|

|

There is one credit card at least that offers no balance transfer fees and has a low purchase interest rate. Plus, there’s no annual fee. That’s the Simmons Visa Card.

But you should note, Simmons Bank only accepts applicants with excellent credit.

Read the Simmons Visa Card editor’s review.

Citi Double Cash: Best for Ongoing Rewards

Citi Double Cash Card Pros & Cons

| Pros | Cons |

|---|---|

|

|

Citi Double Cash offers a lengthy introductory period.

Furthermore, the card offers a simple cash back program that will fit any consumer — all for no annual fee.

Read the Citi Double Cash Card Editor’s Review.

How We Picked

We analyzed more than 80 credit cards offered by U.S. credit card issuers and compared their card fees, interest rates, and benefits.

These cards were ranked based on how each one would best help consumers minimize the amount of interest paid on their card balance.

For full disclosure, some of the cards are from advertisers on MyBankTracker, but they are truly the best cards that we’d recommend even if they weren’t affiliated partners.

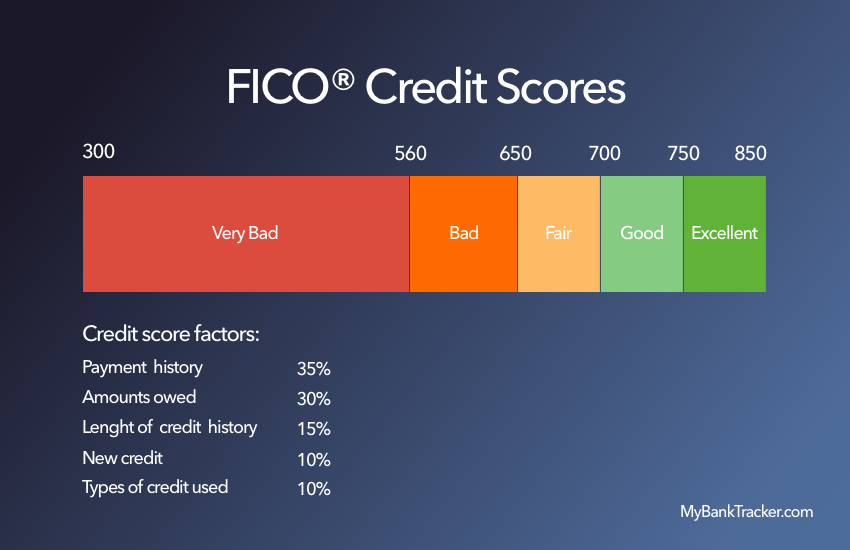

What Credit Score Should You Have

You’re more likely to qualify for a lower interest rate if you have a good credit score. With a FICO credit score of at least 700, you’re in the best position to get lower APRs.

So, if that’s your goal, it’s important to keep credit in pristine condition.

Good credit does not mean an absence of debt. If you have not defaulted on any loans, you can still score well. Even carrying large amounts of debt load may not hurt your chances of approval.

Tip: Keep your credit usage to less than 30% of your total credit card limit to keep your credit score high.

Secured credit cards with bad credit

The alternative for people with bad credit is a secured credit card. It’s mostly the same as a regular credit card, except that it requires a security deposit as collateral.

Normally, the amount of the security deposit is the amount of the card’s credit limit.

Your credit limit, in addition to all activity with the secured credit card, is reported to the credit bureaus. If you practice positive credit behavior, this will help you build or repair your credit.

Generally, if you have bad credit, it’s not a good idea to carry any type of balance on a secured credit card.

But, it’s nice to know that you have a low APR if you ever can’t pay off the entire card balance.

Low APR vs. Rewards Cards

Every credit card exists to create a profit for the credit card company that issues it.

With every purchase on a credit card, the consumer is taking out a loan where the lender expects to earn interest on the amount lent.

How low-interest credit cards work

Low APR credit cards charge low interest rates on balances carried over month to month but don’t usually offer rewards.

In the eyes of credit card companies, low interest rates are appealing to consumers who tend to carry a balance, thus allowing the issuer to collect interest charges.

Pros & Cons of Low Interest cards

| Pros | Cons |

|---|---|

| Usually no annual fees | No rewards |

| Minimizes the interest charges if you carry a balance on the card | Likely to also lack amazing card perks and benefits |

How rewards credit cards work

Great rewards credit cards will award perks such as cash back and points for gift cards and airline miles, but the APR will be rather high.

High rewards are attractive to consumers who are frequent shoppers but do not carry high credit card balances.

Instead, card companies profit from the portion of the card processing interchange fee that merchants pay for every transaction.

Pros & Cons of Rewards Cards

| Pros | Cons |

|---|---|

| Earn rewards on your spending | The top rewards cards are likely to have annual fees |

| Cards may come with premium perks and benefits | Relatively high interest rates |

| Rewards programs may be complex |

Deciding on a Type of Credit Card

The determining factor for choosing a low APR credit card or rewards credit card is your tendency to carry a balance. Minimizing the finance charges on a credit card is the primary goal.

If you expect to be carrying a balance on a regular basis, a low-interest credit card would be ideal.

Earning cash back on all your purchases isn’t financially wise if you are carrying a balance that is charged 15% APR, which compounds to even more interest over time.

If you are diligent in paying off your entire credit card balance month after month, a rewards credit card offers the greatest perks.

It doesn’t matter if the APR is 11% or 15% because by paying off the entire balance, card companies will not charge interest and therefore nullifies the relevance of the APR.

Instead, take advantage of rewards or cash back credit cards.

In a nutshell: If you don’t think you’ll be able to pay off your entire card balance on a monthly basis, you should opt for a low-interest credit card. Otherwise, you may prefer a rewards credit card.

Balance Transfer Credit Cards for Low Interest Rates

Low-interest credit cards can have low APRs for many years to come. But, if you’re trying to tackle your credit card debt right now, balance transfer credit cards may be more useful.

These cards might offer introductory balance transfer APRs that are as low as 0%. Balance transfers can be used to consolidate other kinds of debt (e.g., student loans, personal loans, etc.) in addition to credit card balances.

Tip: To ensure maximum effectiveness of a balance transfer, you should avoid making new purchases or cash advances on the credit card. Those will not only come at a different interest rate than the transfer, but they can also cause you to grow the balance you’re trying to shrink.

When you don’t have to pay any interest on your balance, you can focus on reducing the debt. Plan out how much you have to pay every month in order to eliminate the transferred balance before the introductory period ends.

Note that many credit cards will charge a balance transfer fee. It often costs 3% to 5% of the amount transferred. Be sure to account for this cost.

How Credit Card Interest is Determined

Even the lowest APRs on credit cards may appear high compared to the interest rates on other types of loans.

The reason is credit cards are not tied to any form of collateral. (Unlike the homes and vehicles that are financed by mortgages and car loans that can be taken by the bank in case of default).

The APR for your credit card can vary depending on your credit score. The higher your credit score, the lower your interest rates.

It should also be noted the credit card interest rate that you end up with is calculated by the card company’s formula.

Most commonly, card companies start with The Wall Street Journal’s Prime Rate.

Then, depending on your creditworthiness, card issuers add a certain percentage to that rate. The riskier you are as a borrower, the larger the amount that is added to the Prime Rate.

How to Improve Your Credit Score for Low Interest Rates

To be eligible for low interest rates, a higher credit score will help. Keep some of these tips in mind:

Spend what you can afford

Naturally, debit cards and credit cards differ in one basic way. With the former, you’re spending money you already have in your checking account.

For the latter, the money you spend is not yours; it’s borrowed and must be repaid.

The difference between how the two card types work is what causes credit card debt to get out of control. Sometimes, people forget how much they’ve charged to their credit card.

One solution is to treat your credit card as you would a debit card. Before swiping your credit card, ask yourself one question – “Would I be able to afford this purchase on my debit card without going overdraft?”.

Make a habit of this, and it keeps your credit card balance low, and easier to pay off. It also maintains a low credit-to-debt ratio. Each of these things reflects positively on your credit report.

Make smaller “micropayments” each month

There doesn’t have to be an all-or-nothing approach to paying off your credit card bill. Paying it off in full each due date is recommended. Making partial, late, or zero payments isn’t ideal.

One way to make your balance work to the benefit of your credit is to make smaller payments throughout the month. These payments (also called micropayments) can lower your debt utilization ratio. At the same time, they keep a healthy amount of active credit on your card.

This will also show up on your report as evidence that you’re using your credit card responsibly. Time your payments so that you’ve paid off your full balance by the end of the billing cycle.

Ask for more credit

Asking for a higher credit line does not necessarily result in more debt.

While you’ll always want to keep your debt utilization on the lower end, increasing your credit limit can help boost your credit score. That’s because it shows your credit card provider that you can manage a higher balance. Plus, those low-interest rates stay where they are.

However, if you request an increase, the application process may include a hard check to your credit.

This can ding your score – not a good idea if your credit is low. If you’re confident that it’s in good shape, go for the higher credit limit. The good thing about it is that it not only can boost your credit, but you’re also not obligated to utilize all of it.