The Best Balance Transfer Credit Cards of 2026

Imagine not having the burden of high interest rates on your credit card debt. You can do something about it.

Use a balance transfer credit card as a tool to help you pay off debt faster because it can reduce or eliminate the interest charges on your debt.

You might be able to qualify for an introductory rate of little to no interest for up to 21 months. If you’re approved for a 0% APR balance transfer credit card, you can use the card to pay off your other credit card(s).

Then, you can focus on paying off your balance without interest charges to slow you down.

Find out which balance transfer credit cards are most recommended by us to help you eliminate debt:

The Best Balance Transfer Credit Cards of 2022

| Credit Card | Best for | MyBankTracker Rating (1-5 Stars) |

|---|---|---|

| Citi Diamond Preferred | Best for Entertainment & Leisure | 4.0 |

| Citi Double Cash Card - 18 month BT offer | Best for Ongoing Rewards | 5.0 |

| U.S. Bank Visa Platinum Card | Best for Debt Consolidation With No Annual Fee | 5.0 |

| Citi Rewards+ Card | Best for Rounded Up Rewards | 4.0 |

| Simmons Visa | Best for Ongoing APY Rates | 5.0 |

Citi Diamond Preferred: Best for Entertainment & Leisure

Citi Diamond Preferred Card Pros & Cons

| Pros | Cons |

|---|---|

|

|

The has a lengthy introductory APR period.

Essentially, it’s a great choice for debt consolidation. And, there’s no annual fee.

Read the Citi Preferred Diamond Card editor’s review.

Wells Fargo Reflect Card: Best for Cellphone Protection

The Wells Fargo Reflect Card offers a long introductory APR period that will be very helpful for those who are seeking to consolidate debt.

Additionally, being a Wells Fargo credit card, cardholders get up to $600 in cell phone protection (when your monthly phone bill is paid with the card; terms apply).

The card has no annual fee.

U.S. Bank Visa Platinum Card: Best for Debt Consolidation With No Annual Fee

U.S. Bank Visa Platinum Card Pros & Cons

| Pros | Cons |

|---|---|

|

|

The U.S. Bank Visa Platinum is another great choice for borrowers who are focused on debt consolidation because the extended 0% APR on balance transfers will provide plenty of time to pay down your balance.

This card also doesn’t charge an annual fee. Even better, you don’t have to have a perfect credit score to get this card.

Read the U.S. Bank Visa Platinum Card editor’s review.

Citi Double Cash Card: Best for Ongoing Rewards

Citi Double Cash Card Pros & Cons

| Pros | Cons |

|---|---|

|

|

After you’re done paying off credit card debt with the help of a balance transfer, you might want to keep using the credit card.

offers a great balance transfer introductory offer and it’s also great for ongoing cash back rewards.

It comes with no annual fee.

Read the Citi Double Cash editor’s review.

Citi Rewards+ Card: Best for Rounded Up Rewards

Citi Rewards+ Credit Card Pros & Cons

| Pros | Cons |

|---|---|

|

|

Pro tip: Citi Rewards+ Credit Card is best for rounded up rewards. You can round up the last purchase to $5, and earn 5 points per dollar on that transaction – this means you’re earning more than 1% in value! Plus, there’s no annual fee either.

If you spend 10 dollars a week at your local grocery store with these benefits then it would take just over two years before those who use cash or debit cards pay twice as much in fees (without even accounting for other card perks like miles/points).

Read the complete Citi Rewards+ Card editor’s review.

Simmons Visa: Best for Ongoing APY Rates

Simmons Visa Card Pros & Cons

| Pros | Cons |

|---|---|

|

|

Simmons Visa offers the best ongoing interest rates. Simmons has a great selection of products and services, with competitive APYs for all types of accounts.

It has a low regular APR on purchase and balance transfers.

So it can be used to help consolidate high-interest credit card debt and as a low-interest credit card after you’d paid off that transferred balance.

Read the Simmons Visa editor’s review.

How We Picked

Every credit card is designed for a specific type of consumer. Therefore, not every card is a perfect fit for balance transfers.

We analyzed and ranked more than 20 credit cards available on the market that are popular for balance transfers and compared their card fees, introductory APR periods, card benefits and how the card can best help a consumer through affordable balance transfers.

Note that while some of the cards are from advertisers on MyBankTracker, they are truly the best cards that we’d recommend even if they weren’t affiliated partners.

How Balance Transfers Can Help to Consolidate Debt

As mentioned above, balance transfer credit cards can be useful debt payoff tools since they give you a break from interest charges. But, they’re also great because they can help you consolidate debt.

If you’re carrying balances on multiple credit cards, it can be difficult to track your finances. Plus, if they all have high-interest rates, a large percentage of your payments goes toward interest instead of the principal.

The principal is the original borrowed amount and it does not include interest.

Now, imagine moving the high-interest balances to a single card that doesn’t charge interest for a promotional period. As a result, all your payments during that time will be used to pay down the principal. It’s simpler too — you’re making payments to one balance.

This is why 0% APR balance transfer credit cards can be so helpful. It would be wise to find the card with the longest introductory interest rate and try go get approved with the highest possible credit limits. That’s when your credit scores will be important.

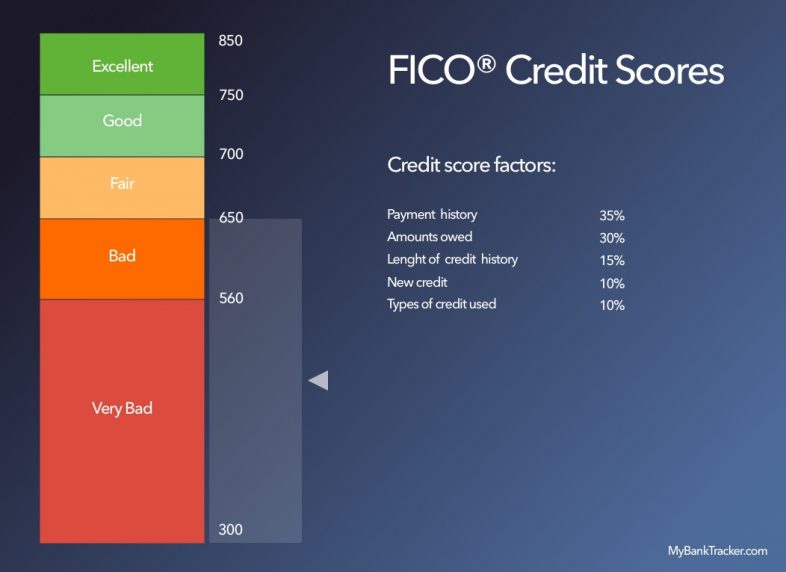

Why Your FICO Credit Score Matters

The standard credit score used by the lending industry is the FICO score, which ranges from 300 to 850. The higher your score, the better.

Credit scores are calculated based on the data in your personal credit reports.

You can get your credit score in a variety of ways, though. More and more credit cards provide free FICO credit scores to their customers. If you already have a credit card, check to see if you’re already receiving monthly FICO scores at no cost.

Credit Score Ranges and Quality

| Credit Score Ranges | Credit Quality | Effect on Ability to Obtain Loans |

|---|---|---|

| 300-580 | Very Bad | Extremely difficult to obtain traditional loans and line of credit. Advised to use secured credit cards and loans to help rebuild credit. |

| 580-669 | Bad | May be able to qualify for some loans and lines of credit, but the interest rates are likely to be high. |

| 670-739 | Average/Fair | Eligible for many traditional loans, but the interest rates and terms may not be the best. |

| 740-799 | Good | Valuable benefits come in the form of loans and lines of credit with comprehensive perks and low interest rates. |

| 800-850 | Excellent | Qualify easily for most loans and lines of credit with low interest rates and favorable terms. |

Get a Balance Transfer Card Without Excellent Credit

Some of the best balance transfer credit cards may be out of reach to those who need them the most. Why? Because they may require excellent credit scores.

The good news is that owing a significant amount of credit card debt doesn’t automatically mean you’ll have a low credit score. As long as you’re making your payments on time, your score could still be in good shape.

Before you apply for any credit card, check your credit score and your credit report.

Tip: Get free credit reports at www.AnnualCreditReport.com (a government-sanctioned website). You’re entitled to one free credit report from each of the three major U.S. credit bureaus: Experian, Equifax, and TransUnion.

It’s important to review your credit reports for errors. If you find any, contact the credit bureau immediately to dispute and fix the error.

This will help your credit score and minimize potential fraud. It’s a good financial best practice for everyone to review their credit reports annually.

Why the Balance Transfer Fee Can Be Expensive

The main drawback of a balance transfer is the fee.

The fee is usually 3% of the amount that transferred and is added to the total card balance. If you’re transferring a large balance, the fee can be high as well.

Few credit cards will waive this fee. Review the card’s terms and conditions to understand the balance transfer policy before you sign up.

What to Watch Out for When Moving Debt Between Credit Cards

- Credit limits affect balance transfer amounts. The credit limit is the highest balance you can carry on your credit card. If your balance transfer card has a lower limit than the amount of the balance you want to transfer, you should ask for a higher limit.Otherwise, transfer as much of your high-interest balances as possible. You can consider another balance transfer card in the future, if needed.

- No rewards on balance transfers. It’s important to note that you can’t earn rewards on balance transfers because they’re not purchases. This also applies to sign-up bonuses that require a certain amount of purchases.

- Balance transfer APR may not be the same as the purchase APR. There’s one for the balance transfer and one for purchases. Make sure to review a card’s APRs so that you’re not surprised by the interest charges that differ based on card activity.

Tips for Using Balance Transfers

Balance transfers aren’t always as simple as moving money from one card to another. Ensure that your balance transfers go smoothly so that you can start working on becoming debt-free.

1. Compare and Calculate Transfer Fees

It’s important to find a card that can still save you money after you account for the balance transfer fee and the balance transfer APR.

The average balance transfer fee is about 3% to 5%. That means if you have a balance transfer of $10,000, you may be stuck with a fee of $300 to $500.

2. Don’t Make New Purchases on a Balance Transfer Card

It may seem tempting to start making purchases on your brand new credit card. That’s what credit cards are for, right?

Not balance transfer credit cards.

Use the card strictly for what it’s intended for: paying down the balance migrated from your other credit card(s). Purchases and any interest charged on those purchases will only hinder your progress.

You could use the card for purchases once you’ve finished paying off the transferred balance.

3. Pay More Than the Minimum Payment Due

With these cards, it’s imperative that you have plan for paying off the consolidated debt. If you pay only the minimum, your debt is likely to not be paid off at the end of the balance transfer introductory period.

What’s worse, you could be charged the new interest rate retroactively on the remaining balance. That alone could ruin any progress that you’ve made.

4. Keep the Card Open

Closing a credit card can hurt your credit score temporarily. Once you’ve paid off the transferred balance, consider keeping it open if it doesn’t have an annual fee.

Consolidating your debt makes paying it off easier, but don’t fall for the myth that transferring your balance is the same as repaying it.